A new year always brings new challenges and opportunities. In 2024, the senior living industry will have plenty of both.

The senior living sector endured a hard year in 2023, starting with multiple stories of operators shutting down or in distress, and ending with assisted living being slammed in the recent Washington Post series.

But there are reasons for hope as 2024 dawns. The industry is heading into the new year with more momentum on occupancy and the prospect of regaining pre-pandemic census levels by the year’s end. At the same time, they are excited by a relatively low rate of new construction starts and looming demand from the baby boomer generation, which could keep occupancy gains flowing into 2025 and potentially beyond.

As it has been for the previous few years, staffing and expenses are likely to remain pain points. Scrutiny from the media and the public is also sure to rise in the coming year as the industry gains a more prominent spot in the U.S. real estate market.

Innovation and evolution will continue, meaning operators must make sure they are keeping up with the times. More new entrants into the industry, coupled with tech including AI, are sure to transform senior living in the year ahead, if only in a gradual way.

‘The great rebalancing’ of IL and AL draws nearer

The senior living sector appears to be undergoing what might be called a “great rebalancing,” which would see assisted living overtake independent living as the most prevalent offering.

It’s been no secret that the senior living industry has seen an influx of needs-based demand in the post-pandemic era – one needs only look at the most recent occupancy report from NIC MAP Vision.

Although “recovery trajectories and timelines continued to be uneven” in 2023, according to NIC Principal Omar Zahraoui, assisted living has helped buoy occupancy results in the past year. The product type added census at a faster rate than independent living in the third quarter of 2023, with occupancy improving by 0.9 percentage points to 82.6%, according to NIC MAP Vision. Assisted living operators in secondary markets have already reached pre-pandemic totals with rates of 84.3% in the third quarter of the year.

“Majority independent living properties house more residents compared to assisted living. Yet, if the high-acuity trend persists, we might see a shift with more residents in assisted living than independent living in the coming years,” Zahraoui told SHN earlier this year.

Some operators across the country – including the nation’s largest, Brookdale Senior Living (NYSE: BKD) – have shifted in favor of catering to a higher-acuity population in 2023 as demand dynamics alter the balance of the industry’s product types. The company is forging ahead with its HealthPlus model, which CEO Cindy Baier said in November “sets the stage for 2024 to be a great year.”

On the flip side, independent living growth has been lower than some companies have hoped. Earlier this year, executives with Ventas (NYSE: VTR) noted “disappointing” performance in some of its independent living assets formerly managed by Holiday Retirement.

National Health Investors (NYSE: NHI) has in the last two years reported similar challenges among the former Holiday communities in its senior housing operating portfolio (SHOP), and CEO Eric Mendelsohn was bullish on the prospect of needs-based demand in the future in August when he remarked that the company was seeing improving fundamentals in needs-based senior housing.

Given the demand at hand – and taking into account that assisted living is still among the senior living industry’s top investment targets – it is likely that more companies will seek to grow and evolve in the space in 2024 and the years to follow. Expect to see more companies making high-acuity and value-based care plays a la Brookdale, or debut products meant to serve a resident population with more care needs.

Pandemic recovery ends, next chapter begins

NIC MAP Vision data shows the senior living operators in the country’s top primary markets could return to pre-pandemic occupancy in late 2024.

This will be as good a marker as any to declare that the pandemic recovery period is over. Certainly, the effects of Covid-19 will reverberate throughout senior living for years to come, and the pandemic has forever altered the landscape. But with occupancies back to their pre-Covid baseline, 2024 will be the year when the focus will shift away from regaining what was lost and toward all that can be gained in the future.

This is not to say that the industry is out of the woods, given the state of other operational metrics like staffing and expenses. However, the oldest baby boomers are slated to turn 80 in 2025, and the immediate demand outlook for senior living has perhaps never-before looked better.

Nearly 60% of respondents to an ASHA survey over the summer were considering a move that potentially included transitioning to a senior living community within the next four years. A total of 92% of respondents to that survey agreed or strongly agreed that remaining independent and self-sufficient was important to them. And, just under a quarter of respondents said they preferred to live in their own home.

That data suggests that senior living operators are well-positioned to capture demand from boomers. The challenge for operators now is actually delivering a product that older adults in the generation will want.

Catering to the boomers will require changing the industry’s long-held paradigms, according to Arrow Senior Living CEO Stephanie Harris.

“The industry has historically done a lot of telling people when they can eat and what they can do, and we’re realizing that doesn’t work for today’s consumer,” she said during a panel discussion at this year’s NIC Fall Conference.

She is also in favor of a more “dynamic” pricing structure that is flexible to many different economic situations.

The concession wars resume

The other side to occupancy gains in 2024 will be how operators achieve them. Taking a cue from the past, it is likely that discounts and concessions will kick into overdrive, or at least come back with a vengeance after a period of widespread rate increases.

For one, it seems as though the industry has picked all its low-hanging fruit in the form of pent-up demand.

“From a marketing point of view, I would call it back to normal while steadily moving up,” said 12 Oaks President Greg Puklicz during a recent SHN+ webinar.

The number of operators offering discounts and concessions has ticked up this year, according to a survey from senior living consultancy Bild & Co. The survey showed that the number of operators tracked by Bild offering concessions grew from 17.9% in the first quarter of the year to 22% in the third quarter. Likewise, the number of operators offering no concessions fell, going from 63.6% in the first quarter of 2023 to 57% in the third quarter.

As operators look to add the last bit of occupancy to hit their census targets, no doubt they will employ price-cutting strategies as they always have. The challenge for the industry in 2024 will be to add residents in a way that maintains rates and margins.

In 2021, senior living providers turned to sometimes-deep rent concessions to get residents through the door. Though that was a product of the pandemic era as much as anything, the ongoing end of extend and pretend and other factors will no doubt put pressure on operators in the new year to hit their occupancy and financial targets.

Luxury senior living levels up

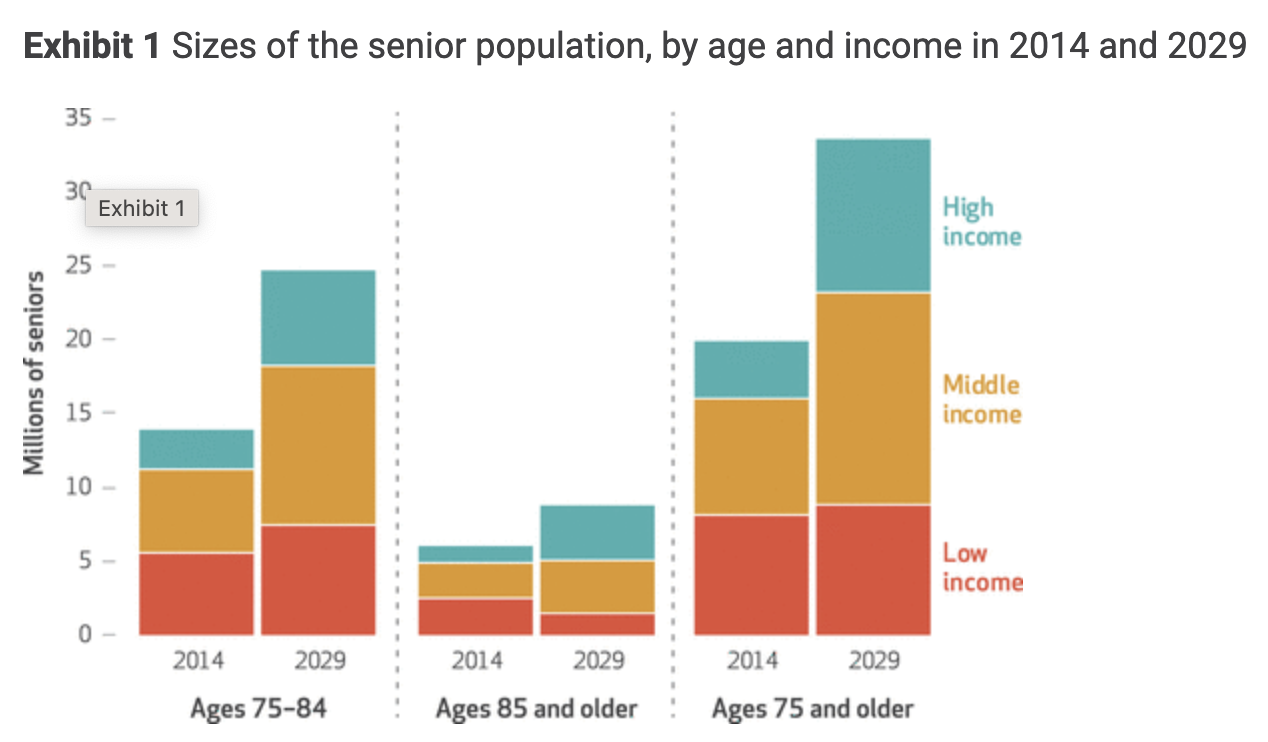

The luxury senior living trend is already red-hot, but it could get even hotter in 2024 – or at least more sophisticated. And this is for good reason. While the groundbreaking “Forgotten Middle” study quantified the huge surge in middle-market demand on the way, that same study also showed major growth in the high-income older adults demographic.

In recent years, companies such as Galerie Living, Sunrise and Vi have all vied for more affluent residents by going bigger on lifestyle and quality of service. Other operators, including Watermark Retirement and Revel Communities, have adopted new membership-based payment structures in order to accommodate resident tastes for the finer things in life.

Luxury senior living has evolved substantially over the last decade, with these and other operators at the forefront. Where the product type was once defined by crystal chandeliers and fine-dining, luxury senior living is now all about a “feeling.” In 2023, it’s becoming less uncommon to see communities with monthly rates in the five-digits and offering world-class concierge services rivaling the country’s top hotels.

Some operators are also now seeing a distinction between what they call “excellence” – providing a good quality service and product – and true luxury, with the latter being a vibe instead of a product to be bought or sold. That distinction is forcing operators in the luxury space to get more savvy about what they are offering and who they are selling to. For example, luxury is a growing trend in memory care, although it looks and feels different than in IL or AL.

As more investors and operators chase a more affluent crowd, more will differentiate themselves by catering to niches or offering services meant to compete with five-star hotels.

Costco Senior Living – or something like it – becomes a credible concept

Just 10 years ago, one might not have guessed that Jimmy Buffet and Mickey Mouse would be big influencers in the U.S. senior housing market. But heading into 2024, they are mainstays among a more active crowd of consumers in search of 55+ housing they can own – and they likely won’t be the only huge brands to make a senior living play in the future.

Since its inception in 2017, Latitude Margaritavilles’ locations have attracted “parrotheads” from all across the U.S., who flock to the communities to buy single-family homes, bask in the sun and enjoy a bevy of party-themed onsite amenities. Latitude Margaritaville President William Bullock told SHN this year that sales have been so hot, the company has had to limit sales each month so it doesn’t “sell more than we can build.”

“While a lot of home builders are cautiously optimistic on the market … we are as bullish as we’ve ever been,” Bullock said in May. “We couldn’t be happier with the space right now, and we’re in growth mode.”

In 2023, the senior housing brand went international, with plans from Mexico-based development group Levy Holding to develop a new property near Guadalajara, Mexico.

Separately, the Storylving by Disney concept developed by DMB Development has had a fast rise since first being announced in 2022. The concept – which was recently extended to a second location in North Carolina – includes space set aside for 55+ dwellings in addition to fun and festive amenities.

In the cases of both Margaritaville and Storyliving, the brands joined forces with seasoned developers and builders, and it does not seem like a stretch to imagine another national brand with appeal for seniors undertaking something similar.

Costco is among the most trusted brands in the U.S., according to the latest Morning Consult Most Trusted Brands survey. Although it’s hard to imagine senior housing dovetailing with a low-cost, warehouse-style retailer like Costco, the company already is involved in a mixed-use development project in Los Angeles that blends a Costco store with multifamily housing. Some apartments will be marketed as affordable housing for seniors, according to the L.A. Times.

Admittedly, this is a far more modest endeavor than the sprawling developments from Disney and Margaritaville. But with developers and operators avidly trying to unlock the secret to middle-market senior housing, a partnership with a brand like Costco makes a lot of sense. Co-locating senior living with a Costco location provides easy access to a vast array of affordably-priced products and services, including groceries, pharmacy and optical care.

Already, Amazon is helping to finance an affordable assisted living community in the Washington, D.C. area. In 2024, expect the line between retail, housing and health care to converge more often and in more creative ways, including in the realm of senior living.

Race for regional density heats up

Two years ago, the rise of regional operators – and super-regionals – was a major trend. Heading into 2024, REITs and other ownership groups still favor strong regional operators, and a race is on to build greater regional density with favored operating partners.

Welltower is one case in point. The word “density” appeared seven times in the REIT’s November 2023 business update. One element of the company’s capital allocation strategy, according to that update, is a “granular approach” that “provides opportunity to acquire assets at deep discounts to replacement cost while complementing Welltower’s regional density strategy.”

An example of this strategy is in Canada, where a number of properties – including communities formerly operated by Revera and Chartwell – will be operating under a new platform created by Welltower and Cogir.

“Planned transitions support Welltower’s regional density strategy within core Canadian markets with Cogir, one of our strongest operating partners,” the business update stated.

The strategy also is in play in California, where Welltower has been methodically expanding its portfolio of communities operated by Oakmont.

Ventas, too, is in pursuit of regional density. CEO Debra Cafaro sees the quest for density as driving consolidation.

“As far as consolidation goes, it’s not necessarily operators coming together, but building a critical mass in markets where they have local penetration … so that they have the critical mass to be profitable and efficient on the chassis that they’ve built,” Cafaro told SHN at the 2023 NIC Fall Conference in Chicago.

The idea is for operators to gain enough scale within these markets to be able to operate efficiently – with the aid of technology – and still have “a sustainable model on a normal, market-based management fee.”

She noted that operators maintaining a minority stake in the real estate of their communities has not created the level of synergy with owners that “people maybe hoped,” and that creating a management model supported by the right level of market density holds the potential to support more aligned frameworks based on annual operating results and NOI growth.

As owners pursue more operator shifts to increase regional density, the operator landscape will continue to change in 2024. Large national players such as Sunrise and Watermark already have seen their portfolios pared back as owners swap in particular operators that they have selected to create density within a specific region. And even some long-established regional operators will be subsumed by other regionals through this type of consolidation. As 2023 came to a close, news came through that RUI is acquiring Brandywine Living.

Working with Welltower, RUI has expanded from its homebase of Virginia to now have communities up and down the East Coast, from Connecticut to Florida. This seems to parallel the growth that Welltower and Oakmont have pursued on the West Coast. Do not be surprised if RUI adds even more communities in 2024 to create even greater density.

This drive for regional density holds the potential to reshape the industry in profound ways, particularly if it does bring about the shift that Cafaro described, away from owner-operator models in favor of next-generation management contracts. And challenges are sure to arise, as it is never easy to do operator transitions – and there are sure to be more large-scale transitions to come in the year ahead.

Greater alignment and operating efficiency are no doubt needed in the industry, but one major question for 2024 could be whether the push for regional density brings about the loss of some long-standing operators that have been industry pioneers – and whether what comes next creates more elevation or dislocation for the sector.

Operators face tougher scrutiny

As the senior living industry becomes more well-known among the general public – and that is the industry’s stated goal – it will no doubt endure much more scrutiny from the press, lawmakers and the general public.

That was on full display in December when the industry was rocked by three Washington Post stories on senior living resident elopement and staffing. The stories centered on residents who wandered from their communities, almost 100 of whom died. The Washington Post reports were hot on the heels of another series from the New York Times and KFF, called “Dying Broke,” about the lack of affordable senior housing

For senior living operators, the stories are a lesson in public relations. They also represent a new hurdle for operators who want to gain the trust of prospects and their families, given that senior living is already fighting against an ingrained negative public perception.

The so-called mainstream media is not the only pillar of American democracy with its collective eye on senior living. Earlier in 2023, Silverado and CEO Loren Shook were charged in a case related to a deadly Covid-19 outbreak early in 2020. Though those charges were later dropped, the case sparked questions about whether prosecutors in other parts of the country might similarly put other executives in the crosshairs.

The bottom line for operators is that the coming years will not be easier with regard to public relations, and they must be prepared to effectively tell their companies’ stories – lest someone else tell them.

The industry also needs to think carefully and strategically about balancing transparency with discipline in 2024 and henceforward. In critiquing the industry’s focus on profits, the Post described a NIC conference session at which presenters “fired fake money from toy handguns labeled ‘MAKE IT RAIN’ when contestants pitched a senior home concept with promise.”

That might seem like a harmless bit of fun to liven up a session, but going forward, industry leaders should consider who might be in the room during conferences, and how they are portraying the industry to people who are casting a skeptical eye over it.

The AI revolution keeps – gradually – unfolding

News headlines in 2023 were awash with bold predictions that an artificial intelligence revolution was right around the corner. But in 2024 that revolution will unfold gradually, and with some setbacks to address and overcome.

That is not to say that AI is not in an exciting trend. In only a few short years, artificial intelligence became a powerful new tool that regular people could use to write prose, code, translate languages and analyze data patterns. Today, it can even be used to help detect mild cognitive impairment in older adults.

But the use case of AI in senior living is still limited. Although many operators tout AI as a way to usher in a new tech-forward future, its current applications are largely rooted in possibility, not practicality.

There is also the fact that some of today’s promising AI functions in senior living are powered by platforms belonging to other actors in the tech space, like OpenAI, which ran into an existential crisis this year after firing and then rehiring CEO Sam Altman. While the saga did not ultimately affect the company’s services like ChatGPT, the entire situation highlighted how controversial and divisive AI technology is, and the serious debates and quandaries that have to be conducted and addressed for responsible use.

Then there are the recent lawsuits filed against UnitedHealth and Humana over their use of AI tools to help determine whether Medicare Advantage beneficiaries should qualify for certain types of post-acute care. These legal battles will play out over the course of 2024, and will help shape and determine the future uses of AI in senior care.

None of this is to say that the senior living industry is not headed toward an AI-powered future – it seems increasingly likely with each passing year that all of us are. And AI was among the hottest topics at our recent BUILD and CONTINUUM conferences, with leaders expressing plenty of enthusiasm about how the technology can already help address major challenges such as fall detection and prevention. But given the barriers that still stand in the way of widespread AI adoption, it does not seem like 2024 will be the year the AI revolutionaries fully storm through the barricades.

Companies featured in this article:

12 Oaks Senior Living, Brookdale Senior Living, Galerie Living, National Health Investors, Oakmont Senior Living, Ventas