Covid-19 has made “density” a dirty word in real estate, and senior living developers are taking heed.

Some data indicate an exodus is occurring from the most densely populated urban centers in the United States, in part because people are wary of coronavirus outbreaks like the one that beleaguered New York City in the early days of the pandemic.

Related to that trend, question marks are hanging over urban mixed-use projects. Prior to Covid-19, such developments were on the rise, in part to meet growing demand for walkable, live-work-play environments. Now, mixed-use density may be less of a feature and more of a bug, because being in close proximity to other people has become less desirable, at least in the near term. And retail, restaurants and hotels are being brutalized by Covid-19 and may take years to bounce back; as a result, expect mixed-use developers to get creative in finding other types of tenants.

One upshot of these trends: Senior living development might accelerate as part of mixed-use projects with a tenant mix more focused on health care, with particular growth in secondary and tertiary markets.

But, the picture is complicated, and some senior living developers have not changed their long-term outlook and strategies, wary of overreacting to what may be temporary disruptions.

The urban exodus

Prior to Covid-19, many of the biggest hitters in senior living were focused on growth in urban markets.

That interest was fueled by consumer demand. Seven out of 10 city dwellers reported that they wanted to live in their current urban environments past the age of 80, in a 3,000-person survey conducted across 10 large cities in 2017. That survey was commissioned by real estate investment trust Welltower (NYSE: WELL), which is the largest owner of senior housing in the United States, and has made urban markets a core strategic focus, including with two high-profile developments in Manhattan.

The urban opportunity also has been fueled by changing real estate market dynamics. Historically, senior housing often was not seen as the “highest and best use” for sought-after urban sites, but as multifamily and other asset classes encountered headwinds in the last several years, that changed. More recently, a slew of senior housing projects have been announced in the nation’s largest cities, including Maplewood’s Inspir highrise in Manhattan; a Brooklyn Heights adaptive reuse project operated by Watermark Retirement; urban life plan communities from the likes of Mather; and a planned $3 billion pipeline of luxury urban communities from Atria Senior Living and Related Companies.

Progress is continuing on these projects and pipelines in the midst of Covid-19, and several industry leaders have reaffirmed their belief in the urban opportunity. Atria still feels “very good” about the plans with Related, CEO John Moore said in May. And Maplewood Senior Living is “steadfast” in its ambitions for future Inspir communities, said CEO Gregory Smith.

Still, Covid-19 has taken a toll on the nation’s cities, and that could affect future senior living development, for better or worse. In particular, the pandemic could hold true for the largest and densest U.S. cities.

“I think that you’re going to see a lot of de-urbanization,” Anthology Senior Living President Ben Burke told SHN. Anthology is the senior living arm of Chicago-based developer and manager CA. Anthology currently operates 27 communities across 11 states and is growing.

One issue is that Covid-19 quarantines are harder to endure for families that are living in tighter quarters in cities, in Burke’s view. Furthermore, many urban amenities are closed while others — including public transportation — present infection risks. Even when the pandemic passes, there is some expectation that companies will allow or encourage more remote working than in the past. This flexibility would also free some people up to move away from downtown office locations.

For some people, Burke observed, “The benefits of living in an urban area are not outweighing the increased price per square foot of urban areas.”

Some data points suggest that a flight from the nation’s largest cities is already underway.

“Early indicators are pointing to an exodus from many densely populated urban centers,” according to the June 2020 National Multifamily Report from Yardi Matrix.

Yardi’s analysis focused on rent growth, which has plunged in expensive and dense “gateway” cities while remaining steady or ticking up slightly in smaller urban markets.

In one example, San Francisco rents were down 3.8% on a year-over-year basis in June, while more affordable markets in California experienced year-over-year rent growth, with Sacramento up 2.2% and the Inland Empire up 2.9%. Midwest markets have also held steady.

“Since January, rents in Indianapolis and the Twin Cities have grown by 0.8% and 0.7%, respectively, and rents in Kansas City have increased by 1%,” the report stated. “These markets have significantly lower population densities than gateway cities and therefore remain attractive, considering social distancing requirements and work-from-home policies.”

New York City was hit hard by Covid-19 in the spring, causing people to leave the city “in droves,” Bisnow reported. An excess of inventory has caused rents to drop across the Big Apple, with average rent in Manhattan declining 6.4% between March and June, according to MNS Real Estate data. Some of the flight from NYC is temporary — for instance, college students leaving while schools are shut down, and more affluent renters decamping to other locations to wait out the pandemic.

Still, Burke anticipates that some people will permanently relocate from New York City and other gateway cities to secondary and tertiary markets that offer enhanced quality of life — think good weather and good schools, including universities. Markets such as Denver; Austin, Texas; and Bozeman, Montana are on his radar.

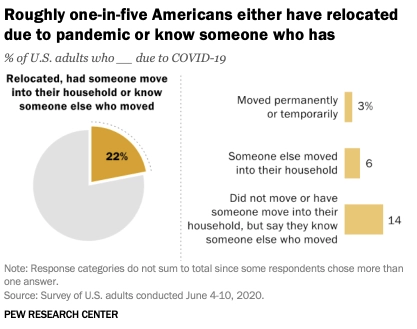

Overall, about one in five Americans moved due to Covid-19 or know someone who did, according to a Pew Research survey in early June. Most people who relocated were young adults; around 9% of people between the ages of 18 and 29 moved due to the pandemic, the research found. That compares to just 1% of people age 65 or older.

However, older adults may eventually relocate to markets where their younger family members moved during the pandemic; this impulse was among the factors propelling population growth among all ages in so-called “hipsturbias” prior to Covid-19. A similar pattern could play out now, particularly as retirees may also find the good weather and more affordable lifestyle of secondary and tertiary markets such as Austin appealing.

“People start to connect the dots,” Burke said.

Despite data indicating pandemic-fueled outmigration from gateway cities, some developers remain bullish on senior living in these markets and are excited by the prospect of new opportunities.

For instance, the hotel industry is critically beleaguered by Covid-19; as hotels are forced to close, developers are eyeing them for senior living conversion projects. Such conversions are a likely route to increase senior living penetration in the New York City metro area, Atria’s Moore and Senior Care Development CEO David Reis recently said.

Underlying the excitement about new senior living development in New York City and other large cities is a belief that the pandemic will not permanently dampen older adults’ enthusiasm for living in these dense urban centers.

“We believe that this experience, while trying and difficult, is temporary,” Brett Gelsomino, Vice President of developer ZOM Senior Living, told SHN.

A mixed-use pivot

While hotel conversions could become a more important route for urban senior living development to occur, Covid-19 has raised questions about the prospects for mixed-use development in cities and the role of senior living within these projects.

Prior to the pandemic, senior living communities were increasingly finding a home in mixed-use developments — including in or near some of the most ambitious projects in the nation’s largest metropolitan areas, such as Hudson Yards in New York City. But, the mixed-use boom was also playing out in other markets across the nation.

Senior living was a good fit for mixed-use urban developments for several reasons, including that families increasingly want their loved ones to live in close proximity rather than in a retirement community on the edge of town, while older adults themselves desire intergenerational environments that allow easy access to good food, entertainment and culture, and public transportation.

Orlando-based ZOM has an active and growing pipeline of senior living projects, and is standing by its “core thesis” to develop urban sites in walkable proximity to a variety of lifestyle and cultural amenities and experiences. Once Covid-19 wanes, Gelsomino believes that people of all ages will be eager to once again patronize restaurants and shops and have other in-person experiences. He would not be surprised if demand for in-person dining and shopping even increases once the pandemic is over.

“In Texas, we’re hearing the term ‘revenge retail,’” he said. “What that means is, people have been locked up for so long that by the time they get out, they almost do it harder than before … If they only went out to eat once a month before, now they’re going out four times a month, because they’ve missed it.”

Indeed, national retail and restaurant spending jumped 17.7% between April and May, as more states began to relax stay-at-home orders. This surge suggests that a significant proportion of people are not deterred by Covid-19 from patronizing businesses.

However, it is also undeniable that the pandemic is walloping certain industries, which will require time to recover, much less expand through new development.

Crowd-sourced review website Yelp has been tracking restaurant closures, which reached 26,160 as of July 10, and 60% of those restaurants closed permanently. As for retail, there is a growing list of bankruptcies related to Covid-19, including such big names as J.Crew, Neiman Marcus, JCPenney and Pier 1 Imports. Anywhere from 25% to 50% of U.S. malls could go out of business, according to projections reported by USA Today. Other types of businesses, including gyms and movie theaters, have also been devastated. Prospects for office buildings are unclear, given the shift to working from home.

With the fate of so many companies and industries up in the air, finding tenants to fill mixed-use real estate development projects could become dicier. In just one high-profile example, Neiman Marcus is closing its 250,000-square-foot Hudson Yards location, creating a “gaping wound” that developer Related Cos. will be hard-pressed to fill, AdWeek’s Diana Pearl wrote.

In this environment, one pivot could be toward mixed-use developments with a health care focus. Such projects were gaining momentum prior to Covid-19, with Welltower CEO Tom DeRosa being a notable proponent.

In-person retail was struggling even before the pandemic, while an aging population presents a growing need for health services; meanwhile, hospital systems have been shifting away from expensive inpatient care toward a more community-based model with “retail-like” locations providing various outpatient services. The resulting opportunity is to create mixed-use projects that are anchored by health care services rather than retail giants — such as Neiman Marcus or JCPenney — as would have been more common in the past.

Examples include Welltower’s Atrium Health project in Charlotte, North Carolina, and a collaboration with Providence St. Joseph to create a wellness center for cancer patients in a shopping center in Mission Viejo, California.

“Now, when you bring someone with you to chemo, they can actually walk across the street and bring you back a Frappuccino or buy themselves a pair of shoes,” DeRosa said in January 2019. Welltower declined to comment for this story.

Covid-19 not only is putting even more pressure on traditional mixed-used tenants but is highlighting the need for health care services, particularly outside of acute-care hospitals that present infection control challenges. Developers are taking note.

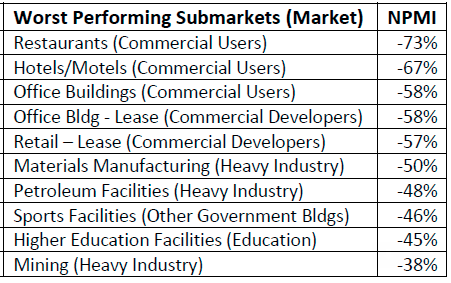

In Q2 2020, health care was one of only four project types that posted an increase in construction proposal activity, according to the net plus/minus index (NPMI) from PSMJ Resources. The index shows the difference between the percentage of firms reporting an increase in proposal activity and those reporting a decrease, with 171 firms participating in the most recent index.

Health care had a +10% showing on the Q2 index; that is down significantly from activity in previous quarters. However, that compares favorably to other types of projects, with the worst performing submarkets including restaurants and hotels.

If health care-anchored mixed-use projects do indeed become more common, senior living communities would appear to be a natural addition.

“As far as medical tenants reentering vacant spaces, absolutely I think that’s a likely scenario, and we have seen that,” Burke said. “I think that’s only a benefit to our projects; any time you can create a continuum of care in and around your [senior living] community is a benefit to the community, to the residents, to the team members, to the family of those residents, without a question … if this is a trend, we would welcome it.”

ZOM’S Gelsomino similarly sees benefits to including assisted living and memory in a health care-anchored mixed-use development, although he thinks that such health-care oriented anchors may add less value to lower-acuity seniors housing, such as independent living.

Gelsomino and Burke also both agree that mixed-use projects with more traditional tenant mixes will not disappear, although they will have to adapt.

The story could be one of increasing division between “haves and have-nots,” as projects thrive if they are in the right markets with the right tenant mix and fail if they do not, Burke said. He is optimistic about an Anthology Senior Living community being constructed in a mixed-use environment in King of Prussia, Pennsylvania, that is anchored by a high-end grocer with a strong regional presence.

King of Prussia’s inclusion of a grocery store that has strong brand equity in the region could exemplify another component of future mixed-use success: a more intense focus on matching tenants to the particular needs and tastes of the local community. Rather than creating cookie-cutter developments featuring national brands, a more boutique mentality could pay off, blending the health care, housing, retail and work needs of a specific consumer base.

As always, developers need to be extremely diligent to find the right location and tenancy mix, Burke said. He believes more affluent markets and projects with higher-end tenants may have a leg up in the near term.

“There’s going to be a flight to quality,” he said.

Companies featured in this article:

Anthology Senior Living, Atria Senior Living, CA Ventures, Maplewood Senior Living, Pew Research Center, Related Companies, Watermark Retirement Communities, Welltower, Zom Senior Living