Now is the time to think big about how senior living can serve a rapidly expanding middle-income market.

“It’s a time to throw spaghetti against the wall,” Beth Burnham Mace, chief economist at the National Investment Center for Seniors Housing & Care (NIC), told Senior Housing News. Mace is a co-author of a newly released research study quantifying the middle-market opportunity.

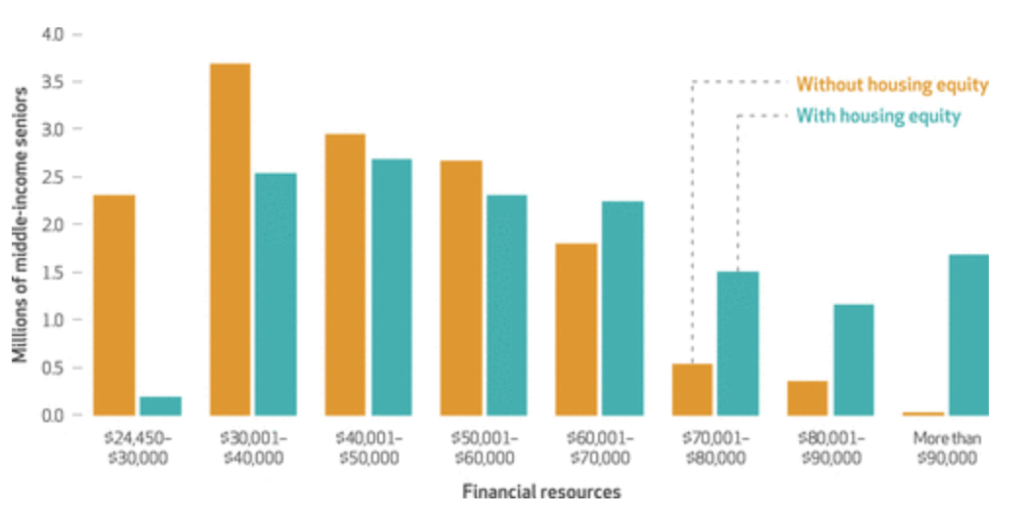

That newly released data projects that the number of middle-income seniors will nearly double to 14.4 million by 2029, and 54% of them will not have the financial resources for private-pay senior living if today’s rates hold. This situation presents a daunting challenge for the country but a tremendous business opportunity for those who can develop the right financing and operating models to serve this demographic.

There were plentiful ideas proposed in the middle-market research paper and associated commentaries published Wednesday in Health Affairs, and at a briefing on the findings held in Washington, D.C.

But Mace also noted that there are some private-pay providers already training their sights on the “forgotten middle” — those people too wealthy to qualify for public programs such as Medicaid but not affluent enough to pay roughly $60,000 a year for assisted living, which is the cost benchmark used by the researchers. If a scalable middle-market model is senior housing’s moonshot, these businesses are willing to lead early missions.

Three such organizations are Lake Oswego, Oregon-based provider Eclipse Senior Living; Washington, D.C.-based developer Capitol Seniors Housing; and Bradley, Illinois-based provider Gardant Management Solutions. Leaders with the three companies weighed in on the new research findings and shared their take on what the future might hold.

Break the mold

The penetration rate for senior housing has held steady at about 10% for years, Eclipse CEO Kai Hsiao told the audience at Wednesday’s Health Affairs briefing. With Eclipse, he is striving to develop a more affordable model to reach the huge proportion of older adults that are not considering a move into senior housing today.

The company was founded in 2017 and manages about 100 properties across the country. Its portfolio is divided into two brands — Elmcroft by Eclipse and Embark by Eclipse. The Embark brand is its foray into middle-market independent living.

The multi-brand approach is inspired by the hospitality industry, where Hsiao began his career. Senior living can glean ideas for middle-market products by looking at how hotel companies cater to both wealthy and middle-income consumers with different development and operating models, he believes.

On the development side, less costly sites and designs are needed to support a lower price point.

“It may be more pre-fab, less urban,” he said.

On the operations side, new approaches are called for in almost every area, from staffing to food and care services. Labor in particular is a sore spot, as wages are on the rise and workers are in short supply across the country, and 60% or more of a standard operating budget goes toward this area.

Creative solutions might include enlisting residents themselves to lead on programming and in other areas, Hsiao and other panelists — including NIC Founder and Strategic Advisor Bob Kramer — suggested.

With senior housing operating margins generally ranging between 34% and 39% as of 2017, it may appear that private-pay senior housing providers can well afford to raise wages and cut rents — and, indeed, a middle-market product might by necessity pull in a lower operating margin, Hsiao conceded.

“With labor being your largest driving force, I think the answer is, regrettably, yes,” he told SHN. “But I think you can negate that by, if you build more units, then you get to basically the same NOI [net operating income] number. So … I can still get to the good revenue number, I just need more units to get there.”

Hsiao also recently predicted that a Medicare Advantage insurer might be the largest owner of private-pay senior housing within a decade, and he repeated that prediction on Wednesday. This plays into the middle-market discussion, because as Medicare Advantage moves to pay for some senior living services, these insurance plans could effectively subsidize the cost of care and enable older adults to devote more financial resources to housing.

While Medicare Advantage-senior living partnerships could therefore be part of the middle-market solution, senior living providers face a challenge to show that they can effectively manage costs and outcomes without being under the direct control of huge insurance companies, Hsiao said.

Threading the needle with active living

The Health Affairs paper focuses on the affordability of independent and assisted living, but the expanding active living sector might be one starting point for building middle-income senior housing options.

Active living communities, also commonly referred to as active adult, provide less health care and can operate with a leaner staff, and are positioned to be on the leading edge of demand as the boomer generation ages. Still, creating middle-market active living communities is no easy task, as Capitol Seniors Housing can attest.

The private equity-backed firm, which has 15 years of experience in acquiring and developing more traditional assisted living and memory care, made a move into middle-market active living in 2017. The strategy is to attract 72- to 75-year-olds at a price point of around $1,800 per month, Founder and Managing Partner Scott Stewart told Senior Housing News, in an interview at the firm’s office on Wednesday afternoon.

But Capitol Senior Housing’s initial active living pipeline has been curtailed, after the company stepped away from three projects that were in the works.

The sites for these projects were very appealing, but once the all-in costs came in — including high construction costs — Capitol realized that rents would have to be nearly double initial projections.

The firm remains committed to its middle-market strategy and did not want to stray from it with these developments. It is under contract for some other active living projects and is actively reviewing possible new sites, which involves a different set of criteria than independent living or assisted living.

AMN

AMN“In assisted living, you want to go into established neighborhoods, go where there are 20- to 30-year-old rooftops around you and find infill locations, suburban locations … here, you want to get ahead of the growth,” Stewart said. “If you do it right, you’re going to not get there too late so land price will be driven up, but not get there too early so that everything is more fiction than reality.”

Some examples of these markets include Alpharetta in Georgia, Loudoun County in the D.C. area, and some markets in the Carolinas and Texas, he said.

Capitol Seniors Housing is also conceiving of an operating model for these communities, including a concierge-like role called a “lifestyle ambassador.” And — like Hsiao — Stewart believes that residents themselves can play a bigger role in creating and organizing programming.

Capitol’s commitment to middle-income active living is based on the large number of older adults in this demographic, and the firm’s belief that there is a lot of runway to grow the portfolio. And Capitol’s math shows that these middle-market buildings should be able to deliver the same strong returns as higher-end assisted living and memory care, although it is more difficult.

“With our partners on the development front, we’re committed to produce to them a levered 20% IRR for all of our investments, and that’s tough,” Stewart said. “It’d be easier if we could shoot for something less than that — call it 15% levered IRR, but we’re at the 20%, so what that means is you’ve got to watch your p’s and q’s from the get-go.”

Land costs, unit count and avoiding “amenity creep” are all keys to keeping development costs to about $200,000 a unit, which enables the target rents. It’s “threading the needle,” Stewart said.

And it remains an open question as to how long active living residents will be able to age in place, Stewart acknowledged. This issue could become increasingly pressing, as the Health Affairs study projects that 60% of middle-income boomers will have mobility issues as of 2029.

Yet, despite these challenges and unknowns, others in the industry also believe in approaching the middle-market opportunity by focusing first on lower-acuity settings.

Ryan Frederick is the founder of SmartLiving 360, which developed The Stories at Congressional Plaza, a 48-unit apartment community in the midst of a mixed-use project in Rockville, Maryland. The all-ages community was built on a universal design model and provides a la carte services, and is meant to attract and foster the wellbeing of active adults in an intergenerational setting. As such, the community is an example of two other ideas for how to create more affordable senior housing: un-bundled pricing and mixed-age/mixed-income communities.

Senior living’s past might hold some keys to its future, Frederick told Senior Housing News. The original operating model of independent living giant Holiday Retirement — a company once led by Hsiao — led to the most successful, largest-scale middle-market offering that the industry has seen, in his view.

That model, which involved community managers who lived on-site, has now been altered and likely is not suitable to be emulated in today’s market, Frederick said, but he sees it as a touchstone.

“Where’s the next Holiday?” he said to SHN, after Wednesday’s Health Affairs event.

For its part, Holiday — which has a portfolio of about 260 communities — still presents itself as an affordable option.

“Almost 50 years ago, Holiday created an innovative and highly successful model for mid-market independent senior living customers,” Holiday CEO Lilly Donohue said in a statement emailed to Senior Housing News. “Recognizing that affordability for retirees is an increasing concern, we evolved in recent years to an even more efficient model to ensure that we can continue as a good value for price conscious seniors.”

Public-private partnerships

A great deal of Wednesday’s discussion in D.C. focused on how public policy and business interests must align if the middle-market senior housing gap will be closed.

There were several suggested public policy changes, including a tax credit for people caring for aging parents, expanding the new Medicare Advantage benefits to fee-for-service Medicare, or creating a whole Medicare long-term care benefit.

Medicaid in particular is a program that holds promise, as it already funds about 10% of senior living today. Gardant is a company that exemplifies how Medicaid is supporting middle-market senior housing.

Most of Gardant’s 56 communities are located in Illinois, where the provider leverages the state’s Medicaid waiver that allows for coverage of personal care, laundry, medication assistance, and a variety of other assisted living services. The waiver is meant to allow low-income individuals to avoid nursing home-based long-term care, which is more costly to Medicaid and less preferred by most seniors.

Gardant’s average monthly rates range between $3,000 in downstate Illinois markets to about $3,500 a month in the Chicago metro area, Vice President of Development and Positioning Rick Banas told SHN. Gardant communities frequently are mixed-income, with about 70% of residents on Medicaid and the remainder private pay.

“I would say the Illinois supportive living model serves as a wonderful model for affordable assisted living that other states should follow,” Banas said.

Gardant is able to hit operating margins of about 32% to 33% if a community is at least 93% occupied, and this is about the average occupancy for its stabilized portfolio, according to Banas. He believes that as other providers have taken occupancy hits due to new competition, Gardant’s middle-market pricing has made its buildings more resilient.

Even though Gardant is posting healthy margins, Banas does believe that investors with more of a social mission angle will be needed for middle-market senior housing to catch on more broadly.

This is NIC’s contention as well, and the organization is hosting an event in New York City next month to present the middle-market findings to the investor community. NIC’s Kramer believes that there is institutional capital that could be drawn to this opportunity.

“One of the largest sources of capital for the middle market is pension funds, which manage the retirement savings of many in the middle class,” he wrote in a Health Affairs blog post. “Fund managers may see an opportunity to meet the housing and care needs of their members, and to achieve the consistent, non-volatile returns that their business requires, by developing instruments designed to finance middle market seniors housing and care.”

Mace underscored this point to SHN, saying, “There are a lot of high-net worth individuals who would be interested in earning a 10% return on something considered socially responsible.”

Others are less bullish on this prospect, seeing misalignment of interests if more public funding enters the picture, and skewed priorities for private-sector investors.

“Increased public financing might be accompanied with additional regulatory requirements, unintentionally discouraging private capital,” Anne Tumlinson, CEO of Anne Tumlinson Innovations, wrote in a separate Health Affairs blog. “I worry that seniors housing operates mostly to create a revenue stream for real estate investors rather than to meet needs of older adults and their families.”

If expanding middle-market senior housing boils down to a choice between more public financing and more private sector investment, Tumlinson has a preference for the public option: de-linking middle-market senior housing from real estate returns might result in more innovative and moderately priced offerings, she wrote.

Banas also flagged the danger of increased regulation as public payers become more involved in assisted living. And there are other risks and downsides.

Illinois’ severe budget woes have slowed Medicaid payments in the past, and although Banas says these issues have largely been resolved, the situation underscores why private-pay senior housing providers are reluctant to hitch their wagons in any way to government payers.

But Gardant is not daunted by its government ties, is currently exploring Medicare Advantage options, and believes that a public-private approach makes sense for expanding middle-market senior living.

“It will take an effort by both the industry and a combination of the government and other entities to get it done,” Banas said.

Companies featured in this article:

Anne Tumlinson Innovations, Capitol Seniors Housing, Eclipse Senior Living, Gardant Management Solutions, NIC