This article is available as part of your SHN+ membership

For years, the senior living industry has discussed creating new models suitable for the middle market. But for all that effort, the industry still struggles in 2024 to meet the needs of middle-income consumers.

When I talk with operators, what I often hear is that it’s just hard to make the math work in the middle market, given the high cost of providing senior living. I also believe that operators aren’t all that incentivized to make their services more affordable. Many are betting they can subsist on demand from more affluent individuals down the road, partly as a way to recoup margins lost during the pandemic.

Although there are some innovative models underway across the country, scalable solutions for the middle market are still lacking – and as I have written before, the clock is ticking. I have long thought that senior living operators have more opportunities to reach the middle market than they think, and that more creativity is required to unlock demand from the millions of middle-income older adults.

A recent conversation with Innovation Senior Living Founder Pilar Carvajal emboldened my view. To Carvajal, senior living operators suffer from a kind of paralysis wherein they are struck by the size of the opportunity and are unsure where to start.

“Part of the paralysis in the industry is ‘Wow, the market is so huge, it could be anything,’” she said. “We have to think very innovatively, but I don’t know if we’re necessarily thinking very innovatively in the industry.”

Still, there are reasons to be hopeful as 2024 gets underway. There’s the recent report from the Milken Institute, sponsored by NIC and CVS Health, that lays out several detailed concepts for how to create more middle-market senior living.

The ideas in the report are exciting in their scope, and we plan to explore them in greater depth in the weeks ahead. But it’s also worth noting that, in addition to the theoretical concepts laid out in the report, the industry also has examples of middle-market models that have already been operationalized and could be adopted on a larger scale. Indeed, NIC also recently shared a case study of one operator’s success in offering more middle-market independent living.

And for all of the industry’s paralysis, Carvajal also thinks operators already have the tools they need to create a scalable middle-market model – and in fact, many such models already exist. The question in her mind is which operators will learn from example and seize the moment.

“In 2024 … there is a lot of interest in this, and I think that we’re going to start seeing a tipping point where things are really going to start to accelerate,” she told me.

In this week’s exclusive, members-only SHN+ Update, I analyze the middle-market opportunity as it stands today and offer key takeaways, including:

- Why the industry suffers from middle-market paralysis

- Why the sector needs to adjust its thinking on public-sector payment sources

- Inside one middle-market model evolving for the future

Avoiding middle-market ‘paralysis’

I can understand the desire to stick to senior living’s bread-and-butter demographic of people who can afford monthly assisted living fees in excess of $6,000. After all, many operators have communities full of such residents.

But Carvajal believes that catering to that crowd is part of the reason the industry struggles with the middle market. Obviously, there is the price barrier, but also the fact that such barriers tell middle-market consumers that these products and services are not for them.

“There’s a huge swath of people that are like, ‘We don’t like you,’ and psychologically, they don’t like us because we’ve said no to them,” she said. “Getting middle-market models out into the market is, I think, going to change the perception of the industry drastically. But we need to start doing it in a big way.”

Part of the danger she sees ahead is that, faced with no other option, older adults may choose less-expensive senior housing options that aren’t suitable for their needs. Or, they might stay at home indefinitely, imperiling their health in the long-term.

For Carvajal, proof that the middle market is within reach can be seen within her company’s eight-community portfolio. The Winter Park, Florida-based company’s operational model revolves around repositioning existing and potentially struggling properties into ones more suitable for Medicaid waiver reimbursement and middle-market plays.

The company’s most recent project includes managing a 97-bed assisted living community in Lake Placid, Florida. Under those plans, Innovation will lease the building and turn it into a middle-market community while getting occupancy and expenses under control.

“We’re taking vintage properties, renovating them with … new paint, new signage, new roof, new flooring; offering semi-private and private options; and allowing for spend-downs into Medicaid if they need it,” she said.

The company also has its eye on Medicare Advantage, and Carvajal said she hopes that one day an insurance product can help pay for services like Medicaid currently does.

Though she believes the middle market is reachable by senior living operators with private-pay models – Innovation and other operators already are operating such communities – she thinks it will take a new way of thinking regarding public payment sources to reach a tipping point as an industry.

That is why she is “testing the theory” that such public-private arrangements are possible and even profitable.

Carvajal is well-suited to test the waters of Medicaid waivers. Her mother, Conchy Bretos, worked as Florida’s secretary of aging and adult services in the 90s, and wrote the state’s Medicaid waiver program. And Carvajal herself spent lots of time hammering out possible models for the affordable senior housing world.

“I had a lot of experience in Medicaid waivers early on in my career, but I also, operationally, got a lot of experience on how to run these tight ships,” she said.

Although Medicaid represents a clear path forward for Innovation, Carvajal does not believe it is the only one worth pursuing, especially given that many states lack strong Medicaid programs. Instead, she sees a swath of models that operators should be testing now.

“When it comes to the middle market, it’s going to be all kinds of things,” she said. “It’s going to be independent living with supportive services, it’s going to be adult daycare, it’s going to be affordable assisted living, it’s going to be technology in homes.”

And for all of her concerns regarding the pace at which senior living operators are moving to meet the market, she also is optimistic about a middle-market “tipping point” ahead, potentially even this year, as Innovation and other companies prove their models can work and generate a profit.

“You just have to be creative,” she said. “That’s what that middle-income senior wants. They don’t want to go to a place to die.”

Model achieves IL rates less than half of competitors

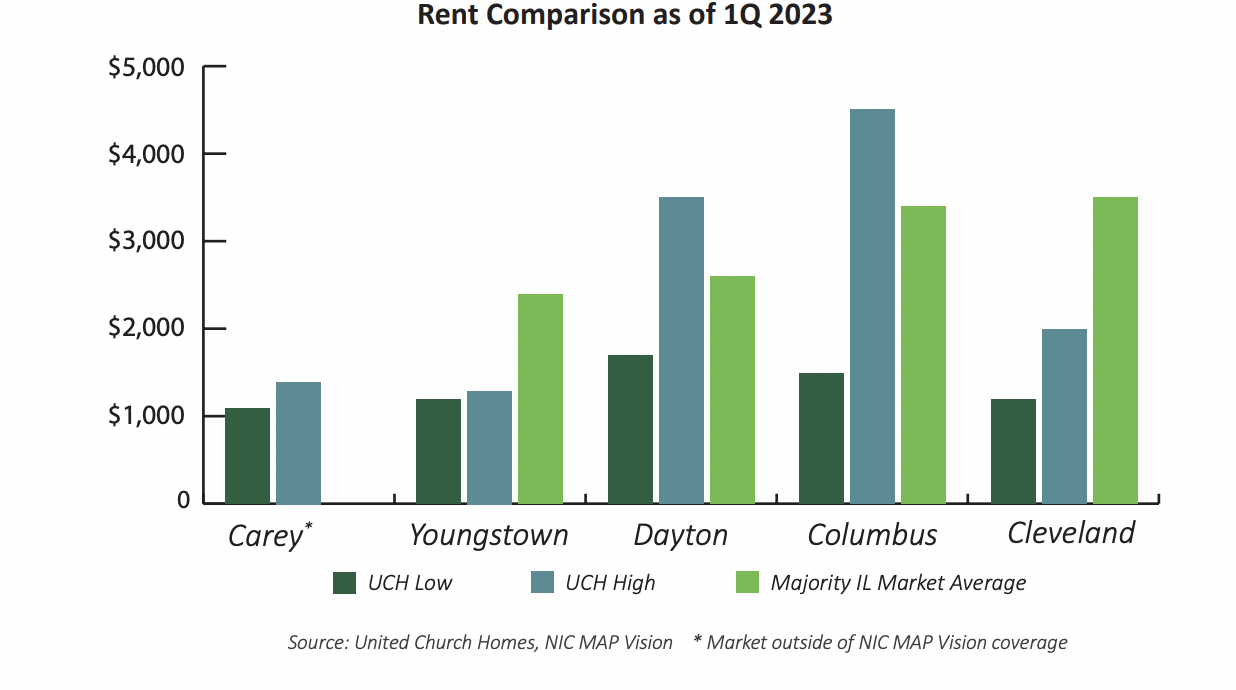

One middle-market model that has garnered attention recently comes from United Church Homes, which is based in Marion, Ohio. The organization has five middle-market communities totaling 450 units, and another five in development or in lease-up totaling more than 500.

A recent case study from the National Investment Center for Seniors Housing & Care (NIC) found that the organization’s model achieves starting rates for independent living that are 53% lower than competitors, on average. And during the pandemic, the portfolio had healthy occupancy rates hovering around 95%.

Although I don’t think the organization’s model is one that every operator can adapt for their own purposes, depending on the real estate they have to work with and the services they offer, it is notable given how the operator has achieved it, and the demand it has garnered by doing so.

Instead of offering one middle-market product for all, UCH offers three based on a resident’s average annual income. Residents who make between $25,000 and $40,000 per year are eligible for a model with monthly rates of just $900 to $1,300; residents who make between $41,000 and $60,000 are eligible to pay between $1,500 to $3,500; and residents with incomes between $61,000 and $73,000 are eligible to pay between $2,000 and $4,500 per month.

Residents receive different services depending on which bracket they belong to, which UCH dubs “low-middle,” “middle” and “middle-high.” On the low end, residents get a base model apartment with essential services and very few amenities. On the high end, they get a model that “looks like a life plan community without an entry fee.”

According to the case study, the UCH middle-market portfolio breaks down into 56% middle, 23% middle-high, and 21% low-middle. About three-fourths of the organization’s projects currently in development or lease-up are geared toward the middle-high bracket, though the case study indicated UCH plans to focus on developing more on middle-income products in the medium-term.

One big piece of the organization’s middle-market puzzle is that it offers home care and dining services in ways that keep the focus on cost control without sacrificing quality.

UCH offers services such as personal care, light housework, errands and pet care in increments as small as 15 minutes, which are much smaller – and more affordable – than the four-hour increments typically offered by home-based service providers.

And given the high cost of food and culinary services, UCH also offers different dining options depending on what residents pay. On the lowest end, residents get no onsite meals but have access to a service coordinator who can aid with meal prep or food delivery, whereas middle-income residents get two meals per day onsite and middle-high get three meals a day, including prepared meals to-go.

Public-private partnerships, smart land use, sharing space with other tenants and leaning on donors for help with development also help fill the gap for UCH.

Using this approach, UCH is able to run middle-market communities with only five full-time employees. That is a stark difference from the organization’s life plan communities, which average 105 full-time employees, according to the case study.

At the end of the day, there will likely be many different factors that help create a healthier middle-market landscape. I don’t believe that the United Church Homes model is one that every other operator can or will use in the future. But I think it illustrates how serving the middle market can be more of a math equation than rocket science, and my hope is that other operators take heed before the demand wave crests – and it is fast-approaching.

Companies featured in this article:

Innovation Senior Living, National Investment Center for Senior Housing & Care, United Church Homes