This article is available as part of your SHN+ membership

Nineteen leaders of senior living operators contributed their thoughts to our annual “Executive Forecast” articles, which we published last week.

These execs provided valuable insights into what lies ahead for senior living over the next 12 months. Their responses covered a wide range of issues and topics, including their operational and growth initiatives, expectations for the economy and top industry trends.

In this week’s exclusive, members-only SHN+ Update, I analyze the executive outlooks and offer key takeaways, including:

- Unpacking mixed messages on labor

- Why operators are going big on renovations, repositioning

- Consolidation, collaboration and a new vision for the middle market

Mixed messages on labor

The good news is that executives generally see labor woes easing, and many operators have notched wins with new workforce-related programs and practices. Here are a few of the comments and stats reflecting these points:

- 12 Oaks Senior Living achieved eight straight months of positive hiring through the end of 2023, and President Greg Puklicz foresees a “restoration to normal scheduling” in 2024

- CEO Chris Hollister reported that Pegasus Senior Living has “mostly rationalized our staffing patterns,” which should help drive NOI in the year ahead

- Vi’s staffing and turnover are back to pre-pandemic levels, as President Gary Smith said the provider “prioritized speed to hire and implemented innovations like a new, unified platform for applicant tracking, candidate relationship management, onboarding, and career site, enhancing efficiency and providing candidates with a more enriching experience”

- Asbury set a goal to achieve a turnover rate of 42.5% and exceeded that by 4%, according to CEO Doug Leidig

- HumanGood CEO John Cochrane observed that “immediate challenges with labor have abated for now,” stated that the organization is focused on “culture, compensation, retention, and professional/career development,” and noted a recent shift from focusing on external recruitment to internal talent development

The bad news — or at least the stark challenge facing providers — is that these positive numbers do not tell the whole story. A thought-provoking dialogue has been unfolding on LinkedIn, spurred by comments that Angie Gray made after reading our executive outlook piece.

She was disappointed that the execs focused so much on “the numbers” and there was no substantive information about how providers are seeking to “grow and develop” nurses and nurse leadership.

“You know, the ones that without them, there would be no senior living,” Gray wrote (while also acknowledging the importance of the various key metrics that CEOs are focused on).

The issue of nurse training and support is of particular interest to Gray, who is a nurse coach and trainer with her own company, High Performance Nursing. But I thought her comments were particularly important in light of the fact that many CEOs who contributed to our executive outlooks said that increased clinical capabilities and care coordination are strategic priorities for 2024 and beyond. Nurses and other clinical leaders will of course be crucial players in driving the success of such initiatives.

I was not alone in taking Gray’s comments seriously. Several leaders within the field replied to Gray with reflective posts. Here’s part of the comment from Bella Groves CEO James Lee:

“The industry regards employees almost exclusively from the lens of shortages, retention and their impact to operating expenses (wages). It’s hardly even veiled at this point that the majority of conversations around employees is how they affect a company’s profitability. I often wonder how frontline leaders and employees feel about things our industry’s CEOs talk about.”

HumanGood CEO John Cochrane acknowledged that in his executive outlook comments to SHN, he did not delve very deeply into the issue of support for nursing teams, as he was trying to keep his contribution more big-picture and brief. But he framed the issue in personal terms on LinkedIn, writing:

“I couldn’t agree more that our field has to pay more attention to this particular segment of our workforce. Perhaps more than any other group, our nurses are overworked and overstressed. If I didn’t recognize this already I got an earful when my RN spouse filled in for some nursing shifts at various HumanGood communities during Covid workforce shortages. She reminded me in somewhat colorful and direct terms of the passion and caring our nursing teams and indeed our healthcare teams overall have for the important work they do.”

And The Springs Living CEO Fee Stubblefield praised Gray’s “provocative comments” and identified the need for greater frontline caregiver support, as nurse leaders delegate to these workers.

In his contributions to SHN’s executive outlook, Stubblefield was one of the few CEOs to paint a troubled picture of the staffing situation as 2024 begins. Each day, workers in the sector are being “rung out, exhausted, broken and many times feeling like failures,” he wrote. He compared caregivers to George Bailey, the main character of the film “It’s a Wonderful Life,” saying that senior living workers carry on out of a sense of mission while doing battle against “their own versions of Mr. Potter,” the movie’s villainous banker and business mogul.

Stubblefield is optimistic that this situation will improve, as ownership groups “will begin to understand how their resources could be better used to take care of people, which will lead to greater financial predictability and returns.”

Yet, Gray’s post and the comments in response suggest that the issue is not only caused by the industry’s Mr. Potters. That is, workers’ exhaustion and feeling of being “broken” is not only the result of having to “carry the burden of a missed pro forma or the weight of analyst expectations,” as Stubblefield put it, but also stem from other issues, including the traumas and trials they have faced through the last three years.

Aegis Living CEO Dwayne Clark in our executive outlook shared that employee wellbeing is “becoming a bigger and bigger issue.”

“Mental health crisis is going up, suicide is going up, and the whole wellbeing issue is critical,” he wrote.

The numbers never tell the whole story in senior living, or in any industry. But in 2024, the improving workforce metrics might belie the situation on the ground in particularly dramatic ways. So, while breathing easier over improved recruitment and retention, providers also need to address the profound issues causing worker discontent and distress.

A year for redevelopment

I was curious what executives would say about construction and development plans, in light of the bearish outlook put forward by several leaders in the last months of 2023.

The overall sentiment toward new development is certainly tempered, with few execs describing major plans and several indicating that construction costs remain prohibitive. Given this climate for green field projects, it makes sense that some companies are focusing on renovating and repositioning their existing portfolios, even launching large-scale, programmatic efforts.

Benchmark and Vi are notable examples. CEO Tom Grape noted that Benchmark has completed a “major renovation” of a “flagship community” and has two other big reno projects underway at other “premier” buildings.

“We will continue our renovation program by beginning a rolling refresh program across a large portion of our portfolio,” he stated. “Starting this year and running through 2025, this project will improve our resident experience and keep our buildings as leaders in their local markets.”

While observing that “lack of development financing … will remain an industry challenge in the near future,” Vi’s Smith touted the company’s ability to maintain momentum on reinvestment efforts, writing:

“In 2024, our Vi communities in Scottsdale, La Jolla, Highlands Ranch and Hilton Head will continue and complete major renovations and remodeling to their common area spaces. Also in 2024, we will complete a $170 million phase of development at our Naples, Fla., community, expanding and renovating our care center venues, and opening 64 new Independent Living homes with entrance fees that average over $3 million.”

Given the increasing obsolescence of senior housing stock across the country, I think that a year or two of intensive renovation and repositioning projects will be extremely timely in preparing for the boomers’ arrival. (We’re interested in reporting on providers that are pursuing ambitious CapEx pipelines this year, and I invite organizations involved in such initiatives to reach out to me.)

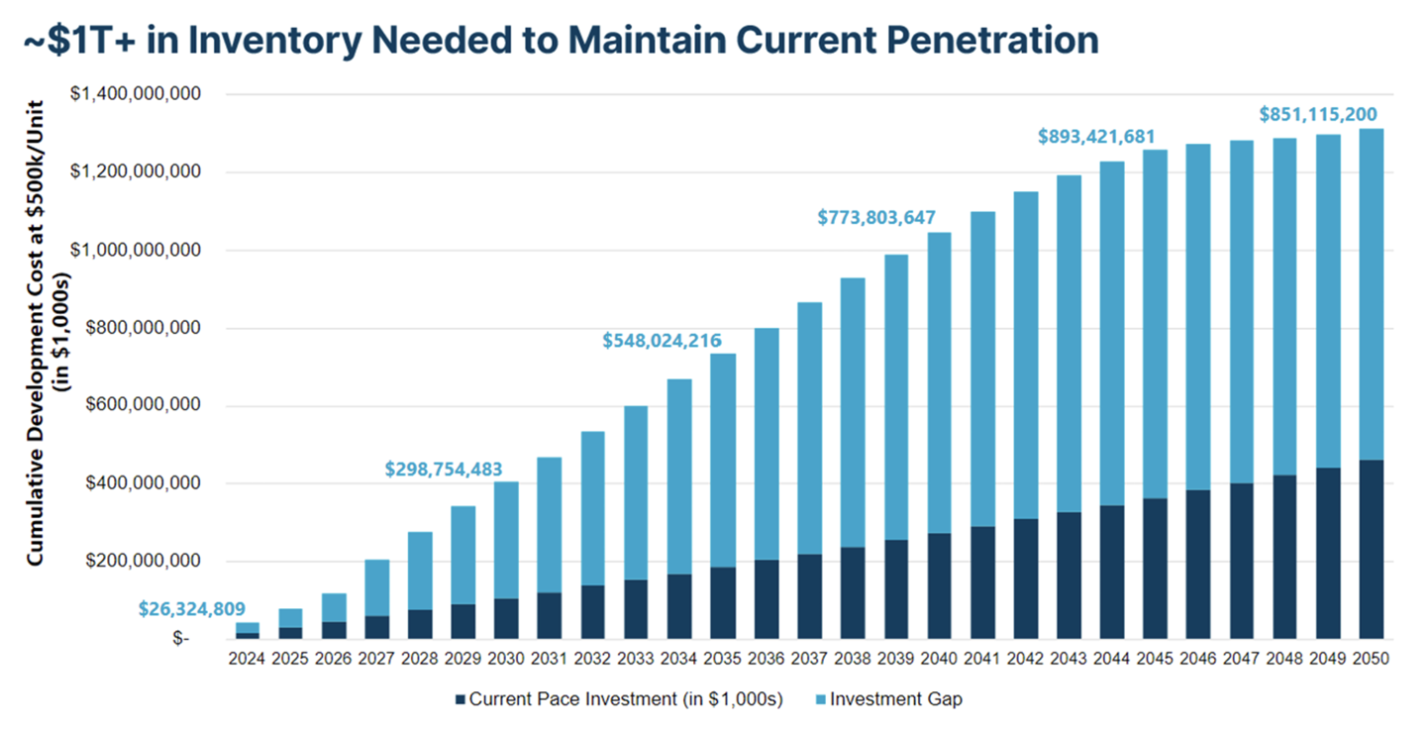

That said, the year also has begun with some angst over the longer-term effects of the extended construction slowdown. Just before New Year’s Day, NIC published data showing that an industry-wide investment of $400 billion in new development is needed to meet anticipated demand, and only about 40% of that investment is on-pace to be fulfilled. About $1 trillion in new development is needed to maintain current penetration through 2050.

There is reason for hopefulness. Several senior living executives — including Grape, Cochrane, Clark and Frontier CEO Greg Roderick — indicated that they anticipate some interest rate moderation in 2024, which would help development to kick back into gear.

And there are some senior living organizations that, even in the current climate, are moving forward with ground-up development, noting the huge incoming wave of demand.

“Even in the face of these difficult market conditions, we plan to invest billions of dollars to meet this demand, maintaining our very selective, disciplined approach, to further expand our national network of communities,” Erickson Senior Living CEO Alan Butler wrote.

Erickson is looking to new markets as part of this expansion, with Butler name-checking California specifically.

Likewise, Garden Spot Communities CEO Steve Lindsey sees indications that access to capital and construction costs could be easing in 2024, and wrote that the organization is looking forward to starting on some new projects in the next 12 months.

“New construction is also in our plans, but we see the future design of senior living being more integrated with the larger community,” he stated. “This effort to blur the boundaries between our campuses and the surrounding neighborhoods will play a critical role in reducing the stigma typically associated with senior living environments. We are also exploring the development of smaller locations that are located in walkable neighborhoods, rather than a traditional life plan community model.”

Whether through renovations or ground-up development, now is the moment for efforts such as Garden Spot’s, to not only refresh old buildings and create new units, but to re-envision what senior living can offer older adults, particularly in light of the lessons learned throughout the Covid-19 era.

As Cochrane put it, “For those willing to rethink, reimagine, and refocus, 2024 will be the year of the Great Restart.”

Consolidation, collaboration and the middle-market opportunity

With development being so difficult, several operator executives flagged acquisitions as their focus for growth in 2024. They see plenty of opportunity, particularly as interest rates, labor costs and other factors continue to create financial distress, and the year could be a big one for operator consolidation.

“The outcomes are likely to include the consolidation of managers and operators,” Stubblefield wrote in his outlook. “Investors are making hard decisions to ‘switch horses,’ and banks are increasingly feeling the weight of the keys in their reluctantly outstretched hands.”

Solera Senior Living CEO Adam Kaplan made a similar point, writing: “Financial demands are untenable due to cost escalation, interest rates, and lack of liquidity. It feels impossible, candidly, to satisfy each stakeholder, which is why operator consolidation will continue to be a leading trend in 2024.”

And Solera is among the operators on the hunt, he noted, with the company “interested in acquiring not only individual properties but high-quality management companies that are synergistic to our core competencies.”

Nonprofits in 2024 are sure to continue their years-long consolidation trend. As Lindsey put it, “We also believe that economic factors continue to move us towards looking for opportunities to increase scale and we see interest in our field for affiliations and acquisitions in order to accomplish that goal. As nonprofits, the challenge is to make that a strategic growth decision and not a survival tactic.”

Frontier COO Kandice Alcorn also predicted “more mergers of operators” in the next year. But she also noted “seeing more collaboration between operators.” Her observation about collaboration came back to me this week as I read the new report from the Milken Institute in partnership with NIC and CVS Health, proposing ideas for how to create middle-market senior living at scale.

The report provides the most detailed vision I have yet seen for how to actually meet the middle-market challenge, and is the product of collaboration among experts from the senior housing sector and beyond, including the worlds of academia and government. And the ideas that these experts generated and put forward in this report call for deep and creative collaboration among senior living operators and other stakeholders.

For instance, the report proposes the creation of an advisory council and senior housing social enterprise. The advisory council would involve “best-in-class middle-income senior housing operators and senior housing-focused financial experts,” and would advise lenders on how to work out distressed and foreclosed properties by repositioning them for the middle market. A social enterprise — such as a land bank or community land trust — would act as an intermediary between financial institutions and senior housing owners and operators. The social enterprise would facilitate a process through which owners and operators would temporarily hold distressed assets, reposition them for the middle market, and then potentially buy the properties or transition them back to lenders.

I find these ideas compelling, but realizing this vision would require impressive levels of collaboration within the industry. Among the next steps identified in the report are the creation of an operator and developer coalition that would be able to repurpose properties while maintaining affordability; the creation of a “standardized health data accounting chart” that would be required for participating properties; and the launch of a pilot involving 10 “vetted middle market senior housing operators” that would take on management of a total of about 100 properties.

What seems clear is that 2024 will be a year of workouts for a large number of distressed senior housing communities. I hope these efforts not only spur consolidation but creativity, and that the industry really does seize on this moment to collaborate in unprecedented ways to meet perhaps its greatest challenge — namely, generating a sustainable and scalable offering for the middle market. If this occurs, the year ahead could go down as a turning point in the history of senior housing.