This article is available as part of your SHN+ membership

Based on a number of recent news reports and research studies, I imagine the public is confused about whether senior living is affordable or out of reach, a good deal or a veritable swindle.

These reports and studies include the article headlined “Extra Fees Drive Assisted-Living Profits,” published in the The New York Times; the Senior Housing National Report for the second half of 2023 from Marcus & Millichap; and the “Housing America’s Older Adults 2023” report from Harvard’s Joint Center for Housing Studies. Senior housing affordability also was a recurring theme at our recent BUILD conference and at the NIC conference.

The takeaways can be head-spinning, with mixed messages coming even from within the industry itself. NIC has been on the forefront of quantifying the tremendous lack of senior living options for middle-income older adults, yet you wouldn’t necessarily have known that from listening to one of the highest-profile conversations at the organization’s recent conference in Chicago.

“This industry has done an incredible job at providing all these services at a great price across the whole socioeconomic scale,” Direct Supply Founder Bob Hillis said, in conversation with former Speaker of the House Paul Ryan. “People say, ‘Well, you’ve done a great job at the top of the scale,’ but most of the places I visit are at the bottom or the middle of the scale … I think they’ve done a really, really good job, and that word hasn’t gotten out as much as it should have.”

Mixed messages about the affordability of senior living are in evidence across the other recent news and research reports as well. In this week’s exclusive, members-only SHN+ Update, I analyze these recent pieces and offer key takeaways, including:

- Assisted living affordability varies significantly across markets

- Public-private partnerships appear inevitable to increase affordability

- Providers should proceed with healthy caution regarding a la carte pricing

Decoding the mixed messages

Of the recent articles and reports on senior housing affordability, the piece published in the New York Times – part of the “Dying Broke” series being jointly conducted with KFF Health News – was the most scathing.

The piece described “highly profitable facilities” that “often charge $5,000 a month or more and then layer on extra fees at every step,” and quoted a consumer who characterized the sector as “profiteering at its worst.”

The Marcus & Millichap report, though brief, offered a different and important takeaway about the affordability of senior living communities relative to other options. While acknowledging that senior housing rents are “demonstrating noteworthy upward momentum,” the costs of home ownership likewise have skyrocketed due to mortgage rate increases.

“The typical mortgage payment on a median priced home has risen to $3,115 as of September, roughly $700 shy of the mean rent in an independent living community. Before the pandemic, that gap was more than twice as wide,” the report stated. “These cost considerations could prompt some older households to shift directly into a lower-service care or life plan community, instead of taking an intermediate step of downsizing.”

I believe the Harvard report provided especially compelling information and suggested one explanation for why the messages are mixed regarding the affordability of senior living: There’s an incredible amount of variability across different markets.

A special section within the report introduced the concept of GAPS households – those in the gap between being able to afford assisted living and qualifying for public support. Most of these households could be described as “middle income.” As the authors explained:

“Focusing on the 97 metros for which NIC MAP Vision data were available, we studied adults 75 and older living alone. We then narrowed this group to those with incomes at or above 50 percent of AMI (a standard benchmark for federal subsidy) but too low to afford all-in-one assisted living in addition to out-of pocket healthcare and miscellaneous costs. Across the metros, 29% of single-person households had incomes in this range.”

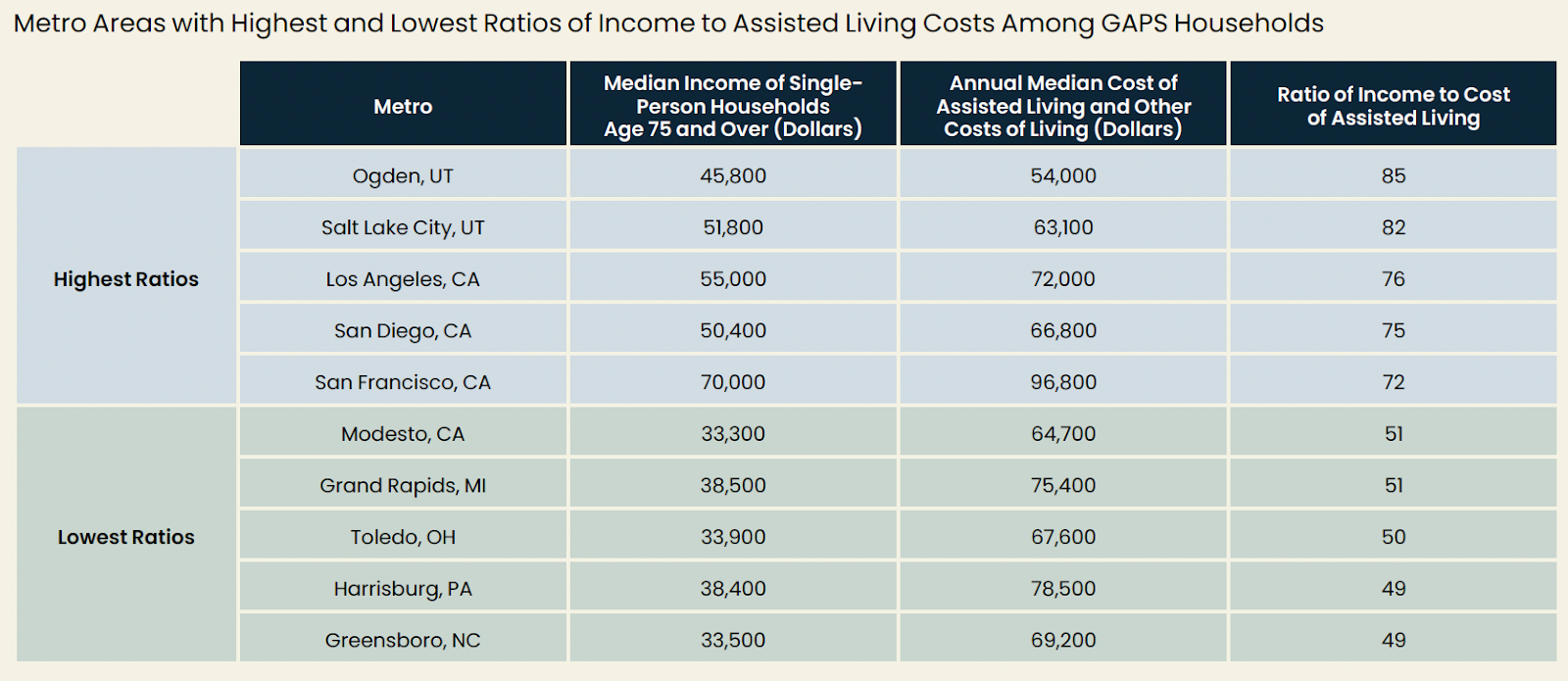

The analysis revealed that across the 97 metros, the ratio of GAPS households’ income to the median cost of assisted living “varies widely.” The average ratio is 62, meaning the typical GAPS household has 62% of the income needed to afford assisted living. But GAPS households are much closer to being able to afford assisted living in some markets than others.

And interestingly, the highest ratios are seen in some of the most expensive housing markets in the United States, including Los Angeles and San Francisco.

“Notably, places with lower-priced assisted living properties are not necessarily more affordable to GAPS households. This is because residents in these metros also have lower incomes,” the report authors wrote.

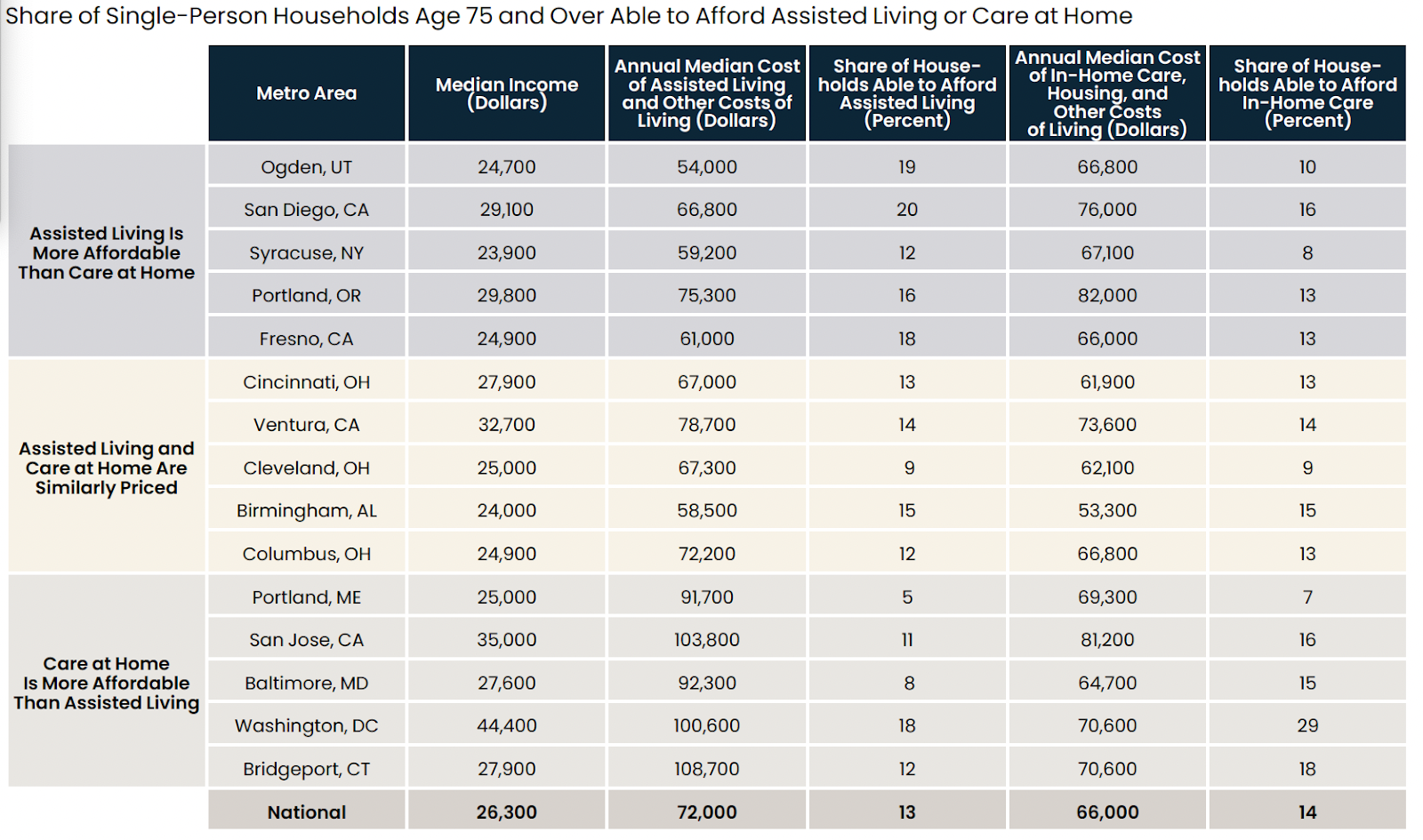

An analysis in the report also demonstrated the variability across markets in terms of whether assisted living or in-home care is more affordable for single-person households age 75 or older.

“Purely from a cost perspective, it is not always clear which service model is more affordable,” the report stated. “Metro-level variations in incomes, the costs of home health aides and assisted living, and the costs of housing, food, and other expenses like transportation and out-of-pocket healthcare mean the calculus varies by market.”

When the subject of senior housing affordability comes up, I often hear owners and operators argue that high rental and service rates do not tell the whole story, and that communal senior living actually is a more affordable option when compared against the costs of homeownership and home care. The Harvard data show that this assertion is true for many places and many cases, particularly if someone needs a high number of in-home care hours – but the data also show that in many places and cases, the math is not so clearly in favor of communal AL.

Compared with the combined costs of four hours of daily in-home care plus other living expenses, the median costs of assisted living were higher in nearly 75% of the 97 NIC MAP Vision markets under examination. And in the 15 markets highlighted in the table above, San Diego has the highest share of GAPS households able to afford assisted living, at just 20%. Home care fares only a little better, with Washington, D.C. having the highest share of households able to afford this option, at just 29%.

I also hear from providers who point to the relatively low rates they are charging, saying this shows that they are serving a middle-market consumer demographic; however, the Harvard analysis underscores how important it is to consider what typical income levels are for older adults in particular markets when determining affordability of AL.

Another common refrain I hear from senior living professionals relates to the substantial home equity that older adults can tap to finance senior living, particularly given the dramatic increases in property values over the last several years. But 28% of GAPS households carry a mortgage, and home equity also is difficult for older adults to access through reverse mortgages, home equity lines of credit, and similar options, according to the Harvard report. And between 1989 and 2022, the share of homeowners age 80 or older with some form of mortgage debt went from 3% to 31%, with the average debt skyrocketing 750%, going from $9,000 to $79,000 in 2022 dollars.

Furthermore, about 25% of GAPS households are renters with no housing equity.

In short, the Harvard report highlights how difficult it is to make any generalized statements about AL affordability, considering the differences among markets and the particular circumstances of GAPS households in terms of their care needs, home equity, and other variables.

I think senior living industry insiders should be mindful about this variability when discussing AL affordability, examine what assumptions they might be making about what financial resources or options are available to a middle-income household, and not lose sight of the key fact, which the Harvard report stated bluntly: “The cost of care is out of reach for most older adults.”

More public-private partnerships inevitable

The inevitability of more partnerships between the public sector and private sector to drive assisted living affordability was another key theme that emerged for me in the recent articles and reports.

Take the New York Times/KFF piece, which is critical of the profit-motive driving assisted living investors and operators. Assisted living shareholders “expect the high returns that are typically gained from housing investments rather than the more marginal profits of the heavily regulated health care sector,” reporter Jordan Rau wrote. And Rau cited an industry survey showing that half of AL operators earn returns of 20% or more, which is “far higher than the money made in most other health sectors.”

However, Rau does not suggest what an appropriate profit margin would be for assisted living, or what mechanism should ensure that AL profits remain within a certain acceptable limit. In fact, I think the article showed how the assisted living sector increasingly embodies the tension at the heart of the U.S. health care system: Is health care an entitlement, or is it a private sector service governed by the rules and principles of a capitalist economy?

In the absence of single-payer health care, the federal and state governments have of course pursued all manner of policies to create a hybrid health care system that blends the public and private sectors. The Medicare Advantage program is one obvious example, with Medicare funds being deployed by private-sector insurance companies whose MA profits are governed by the medical loss ratio.

As assisted living has emerged more definitively as part of the health care continuum, Medicare Advantage has become an important part of the AL model, with providers launching special needs plans, working with primary care providers via MA frameworks, and forming other MA-based partnerships and contracts. The recent Harvard report cited Medicare Advantage as playing an “increasing role” in older adults’ care, as “supplemental plans have had greater latitude to cover services that reduce avoidable healthcare use and improve health for people with chronic illnesses.”

The industry has not rapidly or wholeheartedly embraced the growing role of MA within assisted living, with some providers alarmed at the prospect of assisted living transforming from a largely unregulated sector that can command hotel-like returns to one that is more regulated, with margins dependent at least in part on public dollars. But such a transformation is steadily occurring, and the need for affordable AL options will only accelerate the trend. High-profile articles like Rau’s will add to the momentum for new, more accessible AL models, which might by necessity have profit margins that are more typical for health care.

Medicare Advantage clearly seems to be part of this future, and so too does an expansion of Medicaid for assisted living. After I wrote on this topic recently, I heard from a senior living operator CEO who shared: “One idea that someone raised recently is a CMMI [Center for Medicare & Medicaid Innovation] Demonstration. I think it is an excellent strategy for building a new care model/payment stream in partnership w/CMS that is specific to the senior living industry.”

I think the variations in public-private partnerships will be fascinating and are already proliferating, with another interesting example being the affordable assisted living building that Northbridge Companies and its partners are creating in Washington, D.C., with Amazon as an equity partner. As Northbridge’s top executives explained at BUILD, the Amazon involvement is part of the company’s $147 million commitment to create and preserve affordable housing in D.C. and surrounding areas, where the tech giant located its second headquarters.

“The Residences will be developed by Gragg Cardona Partners, a company that has been working for more than two decades on revitalizing D.C.-area neighborhoods by using public/private partnerships to bring about new investments in housing, commercial space, and community facilities,” D.C. Mayor Muriel Bowser’s office stated about the project.

The Harvard report enumerated several other promising avenues for public/private cooperation to create more affordable housing and care options, including zoning reform and the expansion of low-income housing tax credits, Section 202 affordable housing programs, and Programs of All-Inclusive Care for the Elderly (PACE).

High rates, a la carte pricing demand stellar performance

If innovations in public-private partnerships and other efforts succeed in creating a more affordable assisted living model, that should put an end to some of the horror stories highlighted in investigations such as “Dying Broke” – specifically, consumers bankrupting themselves to access expensive assisted living, as they face a dearth of other options. But another potential problem lies in the disconnect between high assisted living rates and provider performance that can be less-than-stellar.

This is an evergreen concern, of course, but it is an issue that I think will become more pressing for several reasons. One reason is simply the size of recent rate increases in senior living. The increases might very well be justified by surging expenses, but they also give the media a strong angle to highlight lapses in service, safety and staffing – issues that are never acceptable but are all the more damaging to the industry when presented, as in Rau’s article, in the context of providers also charging significantly more than in the recent past.

Then there’s the issue of consumer expectations. Over the last two years, senior living executives generally said that residents accepted large rate increases, given the backdrop of inflation and the need to pay workers more. But several executives also said that higher rates created higher expectations among residents and family members. Providers could be at greater risk of litigation from residents who are paying out hefty sums each month and not seeing their dollars being put to what they perceive to be good use; the NYTimes/KFF article flagged a few suits from recent years related specifically to staffing levels.

Finally, there’s the nuanced issue of how senior living operators are charging for their services. Unbundling has been a trend in recent years, and one that the Harvard report described as a potential way to unlock greater affordability – namely, by only charging older adults for the services that they actually want and need. This was the same point that NIC’s Beth Mace made in the NYT/KFF article, saying that “people want choice.”

But the NYT article presented a more negative – even insidious – take on a la carte pricing, presenting this practice as a way that providers nickel-and-dime residents.

Industry insiders might be riled by Rau’s article, or dismiss it as not fairly presenting the complexities of the business or a full picture of the economics driving the sector. But I think that owners and operators should carefully consider the article’s messaging around a la carte pricing. I certainly can understand why a resident would be overwhelmed, confused, or suspicious of charges calculated through a complicated points system. And insofar as a la carte pricing is still a relatively new practice enabled by evolving technologies that are growing more powerful, providers should be refining their practices and cautious about going too far too fast.

Ultimately, in this period when senior living rates have risen so rapidly and affordability issues are justifiably garnering more urgent attention, providers must be able to answer more and harder questions – from consumers, the press, lawyers and regulators – over whether the services they deliver are worth the prices they’re charging.

Companies featured in this article:

Amazon, Harvard Joint Center for Housing Studies, KFF Health News, Northbridge Companies, The New York Times