This story is available as part of your SHN+ membership

Senior living operators are especially optimistic about the prospect of further occupancy growth in the coming year, at least according to their public comments. But as promising as 2024 seems, I think senior living operators still have a substantial hill left to climb and therefore should not assume that occupancy gains are a given – or that they can be achieved without compromises to the bottom line.

There are plenty of reasons to be optimistic. Average senior living occupancy has steadily risen over the last two years, with an expectation that operators in the country’s largest senior living markets will regain pre-pandemic levels within a year. That is not to mention the fact that the senior living industry is making progress on expenses and staffing, driving up margins as the outlook improves.

But I am also struck by how optimistic operators were at the tail-end of 2022, only to encounter an industry in 2023 that was harder than they expected.

My thesis was emboldened with a recent Stifel note, which noted that the industry is sure to face a “real test” in the fourth quarter of this year and the first quarter of 2024, which are seasonally weak periods for the industry.

“While we are encouraged by the occupancy uptick, the industry has yet to prove that it can significantly increase occupancy through seasonally weak quarters,” the Nov. 19 note to investors reads.

In this week’s exclusive, members-only SHN+ Update, I analyze current and past occupancy trends, including:

- How the industry’s past could inform future trends

- Why 2024 could still be an occupancy slog for some operators

- The threat of price wars as occupancy gains become harder to achieve

‘Real test’ coming for occupancy

On average, occupancy is on the rise as new construction remains low and demand for senior living services remains high. And in recent quarters, senior living operators have reported lots of progress moving in residents and growing occupancy.

During recent earnings calls, leaders of large REITs such as Ventas (NYSE: VTR) and Welltower (NYSE: WELL) seemed confident that their operating partners had a clear runway ahead for occupancy and NOI growth. While I don’t have any reason to doubt their optimism, I’ve heard some of this before.

I recall the optimism that many operators felt at this time last year. For many, 2022 felt like a recovery year from 2021, and there were real hopes and expectations for a return to more normal operations in 2023.

I recall how occupancy optimism was a theme in our executive forecasts at the beginning of this year, and many operators saw the year ahead as a runway for occupancy growth. Multiple leaders shared that they thought 2023 would be an “inflection point” from the challenges of the Covid era to growth and recovery.

To be sure, the industry has made good progress this year. Recent NIC Map Vision data shows that average occupancy has fully recovered in the 68 secondary and tertiary markets the organization tracks. And NIC expects a similar full recovery for the top 31 largest metro areas some time toward the end of 2024.

Even so, the analysts at Stifel still are waiting on results in the fourth quarter of 2023 and the first quarter of 2024, when senior living operators grapple with holiday move-in delays, seasonal influenza and poor winter weather.

And then there’s the fact that even for operators that have recovered occupancy substantially, depressed margins are a challenge to overcome that may require even higher census baselines than in the past. NIC Principal Omar Zahraoui previously noted that “the occupancy level of 1Q 2020 may no longer serve as the benchmark for many operators due to the transformative impact of the pandemic.”

And driving occupancy while building margin could be especially tricky if labor needs also are increasing.

“Margins are recovering, but we believe comps get tougher in 2024 as most of the low-hanging fruit – removing reliance on agency workers – is largely complete,” the Stifel analysts wrote. “As occupancy builds, we also expect operators to have to add additional staff to meet increased resident needs.”

Another issue is that the industry didn’t see as much pent-up demand in recent quarters as investors initially expected, and Stifel’s analysts believe that is driving new concessions and discounting activity among operators who are eager to make up the difference.

“Our guess is that penetration rates increase significantly from current levels mostly due to price discounts for new residents,” they wrote. “If we are correct, we would expect some industry participants to compete aggressively for incremental occupancy by discounting price.”

Discounts and concessions a wild card

If price wars escalate in 2024, I think that could disrupt operational plans that look sound on paper.

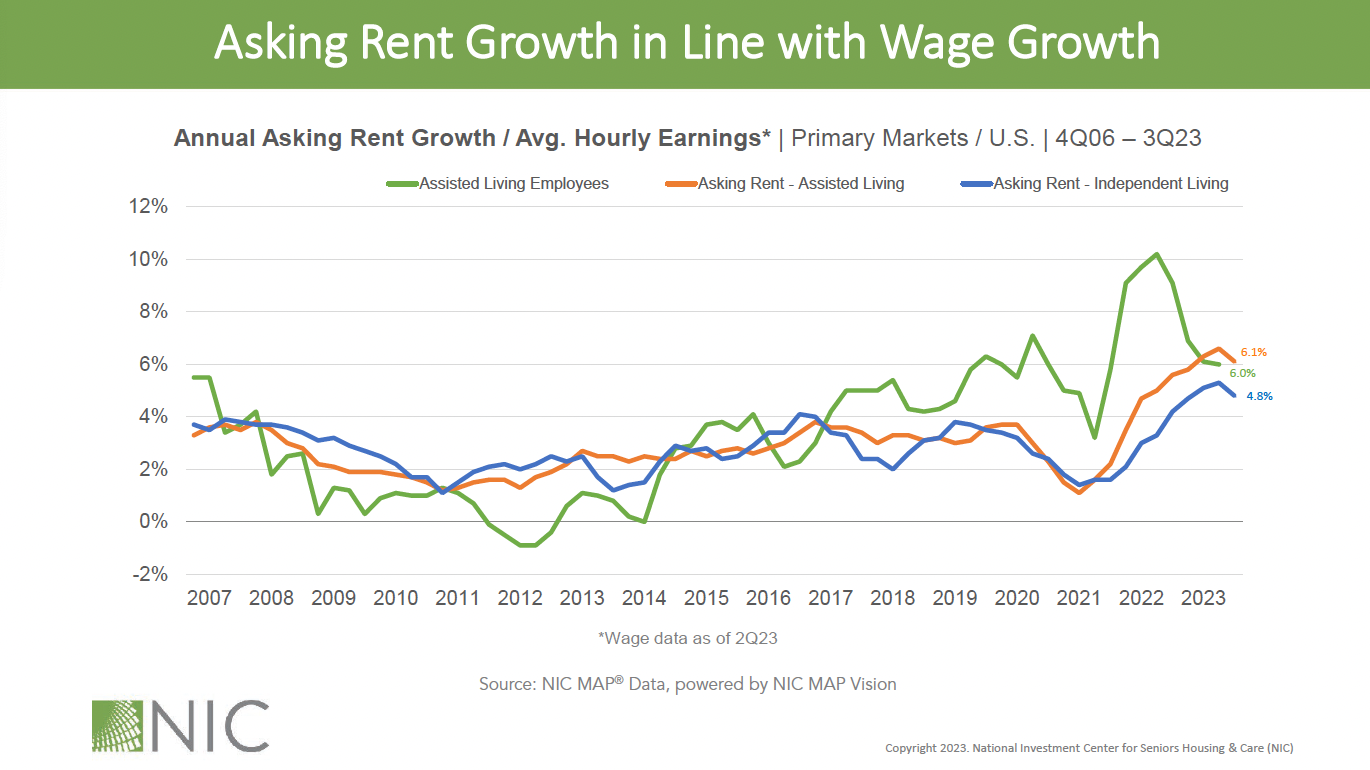

Operators have grown resident rates at a fast pace in recent years, and, asking rent growth has been in line with wage growth, according to NIC data that Senior Principal Caroline Clapp shared at our recent BUILD conference.

Leaders such as Welltower CEO Shankh Mitra remain bullish on the ability of operators serving affluent clientele to keep driving rate. But there are signs that operators will face more pushback on rate increases than they have in the past year or so.

Recent media attention has cast an unfavorable light on cost increases for consumers – the most high-profile case in point being the Nov. 19 New York Times article bearing the headline “Extra Fees Drive Assisted Living Profits.” That article drew attention to the recent aggressive pace of rate increases, and questioned the practice of unbundling charges for various services.

I’m not arguing that providers can or should back off on reasonable and necessary rate increases due to unfavorable press. But at this time last year, providers were almost unanimously telling us that residents were accepting of rate increases, as they understood the extreme inflationary pressures of the moment.

The situation is no longer the same, and it’s worth remembering how quickly some operators historically have been to compete on rate. I think back to the spring of 2021, when senior living operators were enacting deep discounts and concessions to attract residents and regain occupancy lost during the beginning of the pandemic. The coming quarters could provide a stern test of providers’ recent resolve to sell on value rather than price.

And consider that market fundamentals have shifted rapidly in some places. In the beginning of November, NIC’s Zahraoui noted that “recovery trajectories and timelines continued to be uneven, resulting in notable shifts in occupancy rankings among metropolitan markets.”

“Notable shifts include San Jose’s fall from the top spot to seventh and Los Angeles’s steep decline from fifth to 22nd place,” Zahraoui wrote. “These suggest a cooling in California’s once red-hot markets. Conversely, Riverside improved from 23rd to sixth, and Dallas from 25th to ninth, suggesting balanced supply and demand dynamics in these markets.”

Given the prospect of more discounting in some markets, I would not be surprised if, for some operators, 2024 was another year of slower-than-hoped growth and recovery. And while the national trendlines are moving in the right direction, that may mask strife in certain markets across the country.

Companies featured in this article:

National Investment Center for Senior Housing & Care, Stifel, Ventas, Welltower