Rental active adult communities were among the senior housing product types with strongest growth rates, prior to Covid-19 — and the segment proved to be very resilient throughout the pandemic.

Active adult communities generated more interest from prospective renters, compared to independent living. Sales and marketing teams spent less time converting leads into move-ins. And the tenant demographics trend younger and healthier than traditional independent living residents.

But there are questions surrounding how the product, still relatively new to the space, will evolve to meet future demand as more baby boomers retire and age in place within active adult settings.

These were some of the takeaways during a panel discussion at Senior Housing News’ 2021 Active Adult Virtual Summit, featuring Beth Burnham Mace, chief economist for the National Investment Center for Seniors Housing & Care (NIC), and Alex Fisher, president and co-founder of senior living sales and technology company Sherpa.

In many ways, the active adult cohort is taking over the role independent living used to play in the care continuum 20 years ago.

The typical active adult consumer falls in an age range of 75 to 82 years. But a 75-year-old today is relatively healthier than a person of identical age a generation ago. Moreover, their life experiences are different, Mace said. Many boomers turning 75 today have gone to college, traveled, and lived in other communal settings such as dormitories or apartment buildings.

That experience, coupled with demanding tastes, will help inform the layout and scale of future active adult communities, intended to encourage socialization and engagement between residents.

“We’re going to see a different product, appealing to people who want to live in groups,” Mace said.

Pandemic resilience

There are a few reasons behind active adult’s resilient performance during Covid-19.

First, communities were not subject to lockdown protocols that affected higher acuity care settings and independent living, because active adult as a real estate class is similar to multifamily housing and therefore does not require licensure, Mace said.

Many active adult operators reported stronger occupancy and move-in rates than their higher acuity counterparts. Communities tracked by Sherpa averaged nearly four new move-ins per month last year — and communities in the top 90th percentile of performers averaged six move-ins per month, Fisher said.

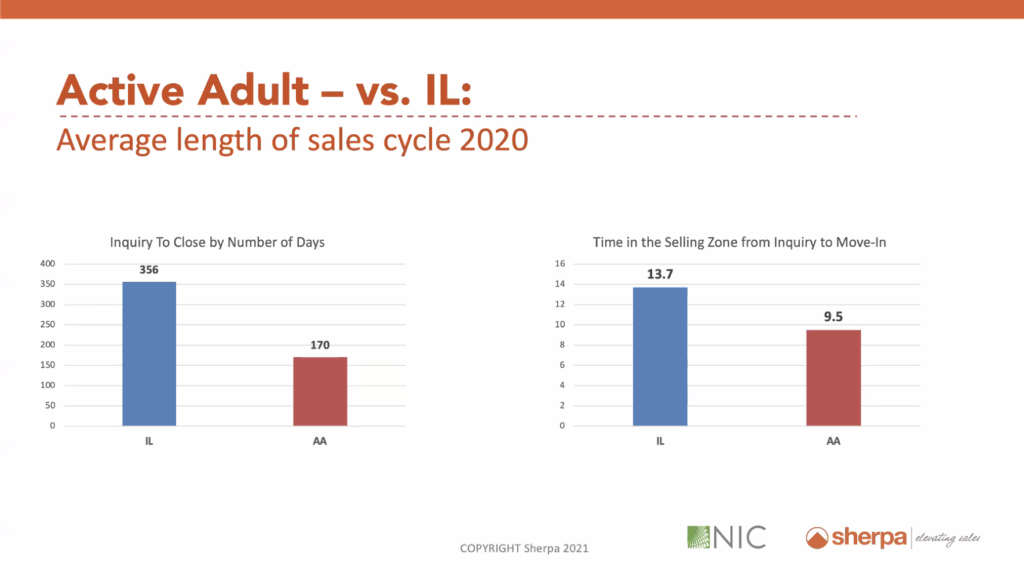

Tour-to-move-in conversion ratios among active adult communities, meanwhile, improved from 30% in 2020 to 35% to date in 2021, according to Sherpa data. Most impressive, the average sales cycle for active adult communities is faster than in independent living. In 2020, the time frame from inquiry to closing a rental in an active adult setting averaged 170 days, compared to 356 in independent living.

And the time active adult salespeople spent in the selling zone, from inquiry to move-in, averaged 9.5 hours to 13.7 hours for independent living.

Community leadership played an essential role in converting inquiries to move-ins, as well. Executive directors at active adult communities did not have to deal with constantly changing restrictions on their communities from federal, state and local public health departments, allowing them to spend more time working with salespeople, converting leads.

“They were able to dedicate more time [to assisting sales teams],” Fisher said.

The resilience is expected to continue in coming years, due to the sheer volume of baby boomers reaching retirement age in the coming decades. The growth among the 75-plus population is expected to increase from 29 million in 2025 to 45 million by 2040. Population growth among the 75 to 84 age demographic — currently the sweet spot for active adult renters, Mace noted — is expected to reach 21 million by 2025, and 31 million by 2040.

Developers in the space will find themselves with opportunities to build newer communities, but need to be mindful of the product type. The lease-up period for active adult may be faster than independent living, but it is slower than traditional multifamily apartments, which is a main competitor for renters. Once stabilized occupancy is attained, however, owners will realize longer lengths of stay among tenants, as well as a rent premium compared to multifamily.

“It really is a chameleon product. It’s still evolving,” she said.

Addressing future acuity creep

While the immediate benefits that active adult communities present are attractive to investors and operators, they also need to keep in mind potential future drawbacks and challenges.

Notably, the probability for acuity creep is heightened because of the longer length of stay. Although the product is relatively new, many active adult communities are already taking over the role that independent living played in the care continuum 20 years ago — without the service components that make independent living attractive.

There are concerns of what will happen to active adult renters as they age and need more services, Fisher said. Developers and operators need to anticipate those needs and look for ways to provide support for their tenants in the future.

One option may include a la carte or unbundled services, offered for additional fees, creating an “independent living light” model without fully morphing into independent living. Fisher believes this is inevitable.

“We can become more flexible in how we offer services and how we charge for them, anticipating the needs of individuals that are going to [need them] — that’s going to happen,” she said.

Mace agreed that the players in the active adult space should be proactive in addressing acuity creep, given the sheer numbers of over-75 boomers gravitating to senior housing in the coming years. What she believes is certain is the demand for choice that is a hallmark of the boomer generation can be part of the solution.

Active adult operators can partner with operators that offer higher acuity care, creating a pipeline of residents that will eventually need assisted living services, and cementing active adult communities in the care continuum.

Or operators can partner with health systems to offer clinical services for residents, which many assisted living providers are already exploring via Medicare Advantage plans. Mace believes these alternatives can be mutually beneficial for all stakeholders. Residents receive health care on site. Operators can free up time for staff to maximize the building’s value proposition. And the health care provider has a captive audience in residents.

Mace also sees opportunities for co-locating active adult communities next to traditional senior housing developments, placing the full continuum of care on one site. These are options developers and operators should consider as they plan new communities, especially as they court new, younger customers to fill vacancies and might be dissuaded from moving because of acuity creep.

“I don’t think we should bury our heads under the rug. [Operators] should be more open about what happens when you age in place,” she said.

Companies featured in this article:

National Investment Center for Seniors Housing & Care, Sherpa