The trend of nonprofit senior housing affiliations snowballed in 2019, and smaller providers now are more motivated than ever to initiate discussions with larger groups. And, more nonprofit providers are diversifying their service lines in order to provide care to seniors off campus.

These trends are on display in the 17th annual LZ 200 list of nonprofit providers from industry association LeadingAge and investment bank Ziegler. The list ranks the largest not-for-profit systems providing aging services through senior living in the United States, in order of total owned market-rate units, as of the end of 2019.

The report reflects LeadingAge and Ziegler’s ongoing commitment to capture a larger representation of the not-for-profit senior living marketplace, Ziegler Director, Senior Living Research and Development Lisa McCracken told Senior Housing News.

The top 10 largest organizations by count are:

- National Senior Campuses – 20, 917 units

- The Evangelical Lutheran Good Samaritan Society – 15,507 units

- ACTS Retirement Services – 9,582 units

- Ascension Living – 8,129 units

- Presbyterian Homes and Services – 7,958 units

- Trinity Health Senior Communities – 5,715 units

- HumanGood – 5,474 units

- Covenant Living Communities & Services – 5,228 units

- Lifespace Communities – 5,179 units

- Benedictine Health System – 4,394 units

The nonprofit senior housing cohort has lost market share over the years as for-profit operators and a wave of new investors enter the space seeking opportunities for growth, including new ground-up development. The nonprofit sector, instead, has focused its construction attention on campus expansions, primarily through the addition of new independent living units. Many providers are also disposing of freestanding skilled nursing facilities, repurposing these buildings into memory care facilities or closing them outright, particularly in rural markets.

“Expansions are one thing that the nonprofits continue to do, and do well,” McCracken said.

Affiliations explode

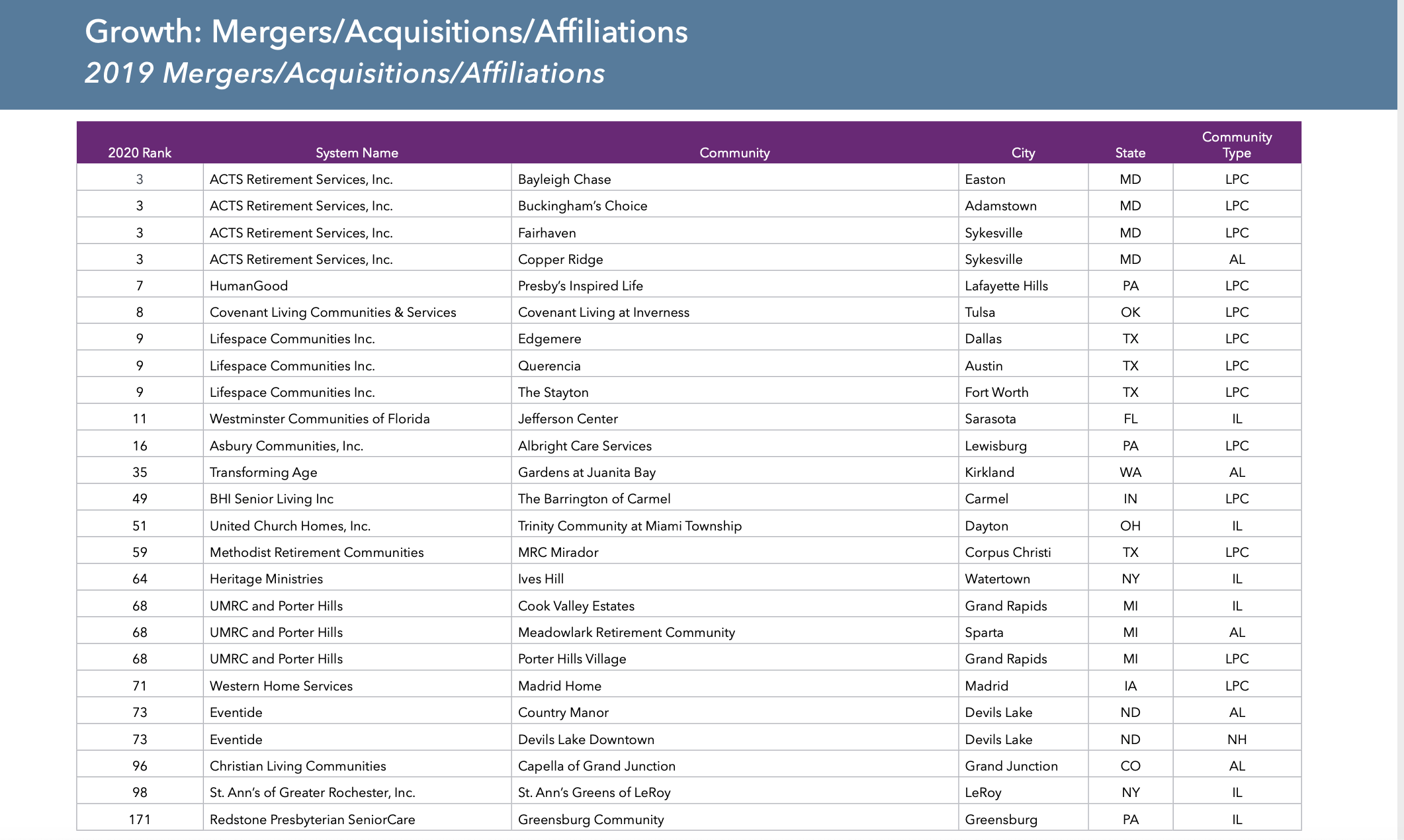

Affiliations between nonprofit providers have built momentum in recent years, but 2019 saw the most affiliations in recent memory: This year’s list reports 25 organizations that grew through affiliations, compared to 10 mergers/acquisitions/affiliations in the previous year’s LZ report. Among the more notable mergers, Acts Retirement-Life Communities announced an affiliation with Integrace in January 2019, giving the Fort Washington, Pennsylvania-based nonprofit an expanded East Coast presence. HumanGood affiliated with Presby’s Inspired Life in June 2019, giving the Pleasanton, California-based operator a foothold on the East Coast. Lifespace Communities and Senior Quality Lifestyles Corporation completed an affiliation in May 2019. And United Methodist Retirement Communities (UMRC) and Porter Hills Presbyterian Village merged in March 2019.

Another affiliation, between Presbyterian Senior Living and Westminster Communities of Florida, fell through in July 2019.

As for-profits pace new developments, nonprofits have embraced affiliation as a catalyst for growth, Ziegler President and CEO Dan Hermann told SHN. Larger providers and their smaller counterparts recognize that affiliations create the ability to build deeper and more experienced leadership teams, and put the merged providers in a better position to benefit from economies of scale and to identify future growth opportunities.

Smaller providers are often the ones initiating affiliation discussions – a trend that has accelerated during Covid-19. Ziegler averaged one strategy session with a smaller provider per week, prior to the pandemic. Now it is averaging two per week and will have conducted 12 strategy sessions by the end of October.

“Smaller organizations won’t wait too long to pursue joining [larger providers] because, if they wait too long, sometimes they’re viewed as too risky to the larger organization,” Hermann said.

New service lines growth

Nonprofit providers are also embracing launching new home and community-based services (HCBS), such as home health care. Roughly half of the entrants on the LZ 200 have some form of HCBS platform, and the larger networks are leading the charge, McCracken told SHN.

Roughly one-third of the LZ 200 offers home care services, which is less complex than home health care or hospice services. One in 10 providers offer a form of continuing care at home program, and 7% have a Medicare/Medicaid-based program of all-inclusive care for the elderly (PACE).

HCBS lines were not tracked by Ziegler and LeadingAge for the report until three years ago, but the data collected since then indicates the platforms hold substantial potential for growth. Ziegler’s data indicates that providers are creating diverse HCBS platforms, often in joint ventures to mitigate risk. These platforms have different staffing patterns and the margins are different than operating a continuing care retirement community. A joint venture allows the provider to share in the profit while the partner provides the services.

“To really grow into scale, that business takes commitment,” McCrackensaid.

In some examples of this diversification trend, Ohio Living is finding success in its home health and hospice arms during the pandemic, and is launching a new physicians services line. Another nonprofit provider, Immanuel Lutheran Communities, is developing a home health care segment to provide services for seniors who are not ready, or unable, to transition to senior housing.

Hermann cited Holland Home, a provider in Grand Rapids, Michigan, as a “poster child” for building a successful HCBS platform. Holland Home is very aggressive in seeking out partners to provide off-campus services and grow its platform to serve as many seniors as possible, and its future growth trajectory includes expanding its HCBS platform faster than brick-and-mortar expansion.

But the opportunity to build a platform of HCBS varies by market. Larger operators in dense metropolitan areas have an advantage over their smaller counterparts, due to their scale and ability to provide services that connect in an organized way. Hermann compares this to how health systems have consolidated in recent years.

“The pattern we see is [providers] thinking about this footprint of the brand in that market, and how that brand can serve more seniors through either bricks and mortar or HCBS,” he said.