Private equity investment in senior housing has gained momentum over the last several years and could reach new heights in 2020 — which might spell trouble for the industry down the road.

Specifically, some private equity funds may be coming to the space for the first time with unrealistic expectations, which could result in a variety of unwelcome outcomes. In one scenario already playing out in some instances, PE owners are pressuring operators to drive short-term results at the expense of long-term viability, in order to generate returns on tight timelines that are standard in other types of PE real estate investment.

For instance, a number of private equity funds are struggling to generate returns in the multifamily space and are eyeing senior housing, according to Mike Gordon, senior managing director and head of transactions for Chicago-based PE firm Harrison Street.

“There’s going to be a bit of a rude awakening when they realize that the three- to four-year hold period in the multifamily space just doesn’t translate in our sector,” he told Senior Housing News.

On the other hand, the influx of private equity is part of a larger diversification of senior housing capital sources, which has been a key objective pursued for many years by industry leaders, particularly the National Investment Center for Seniors Housing & Care (NIC).

Thanks to this diversification, operating companies now have more opportunities than ever to align with the right capital providers — including private equity — to secure their future, but the pressure is on to make shrewd decisions about who to partner with in an increasingly complex marketplace.

The rise of private equity

Private equity funds began to take senior housing more seriously about 10 years ago, in Gordon’s view. Coming out of the Great Recession, investors were looking for more defensive sectors and noted that senior living had held up well in the downturn, as a needs-based product.

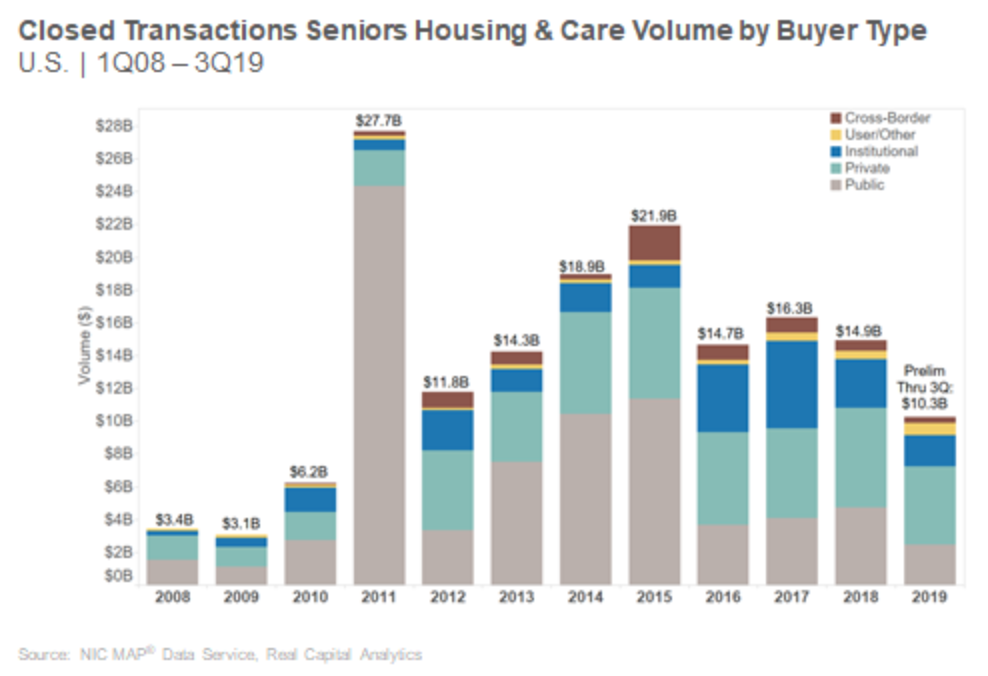

However, public companies such as real estate investment trusts (REITs) dominated the senior housing acquisition market from 2011 to 2015, according to data compiled by the National Investment Center for Seniors Housing & Care (NIC). It was just four years ago that the REITs took a step back, becoming net sellers of senior housing as they sought to reduce leverage and rationalize their portfolios after years of major acquisitions; private equity stepped into the breach.

Private buyers, including but not limited to private equity, have averaged $1.5 billion in volume per quarter since early 2016, according to NIC. This group accounted for 49% of total deal volume in Q3 2019.

“From an investor’s point of view, seniors housing provides portfolio diversification,” NIC Chief Economist Beth Mace told SHN. “And for the institutional-quality operators, we’ve seen that they generate relatively significant investment returns.”

With the demographic wave of aging baby boomers drawing nearer every year, senior housing is almost certain to maintain its attractiveness to fund managers, as reflected in headlines related to funds targeting the sector, many of them raised by companies that have already been active in senior housing for years. A $2 billion KKR fund, a $1.5 billion Bain Capital fund, a $1.6 billion Harrison Street fund, a $1 billion Apollo Global Management fund and a $1.2 billion Kayne Anderson fund have all been earmarked at least in part for senior housing. Other groups, such as PGIM Real Estate, are also active.

But those numbers reflect an overall private equity sector with historic amounts of cash on hand. Going into 2020, private equity firms had a record-high $1.5 trillion in unspent capital, according to Preqin data cited by Bloomberg.

“I certainly don’t have any numbers on this, but I feel like every time I turn around, I read an article about new funds, new money,” Julie Ferguson, senior vice president and sector leader, senior living at Ryan Companies, told SHN.

Prior to joining Ryan Cos. in late 2019, Ferguson was a director with Titan Development; she helped lead that Albuquerque-based organization into the senior housing space and also headed up the firm’s first real estate equity fund, of $112 million. In addition to the billion-dollar funds from heavyweight players, the increased flow of private equity into senior housing is also coming from players on this smaller scale.

Operators under pressure

Going into 2020, this influx of private equity into the senior housing industry is a top concern for Lynne Katzmann, CEO of Bloomfield, New Jersey-based provider Juniper Communities. Juniper itself is not owned by private equity, but Katzmann is troubled by potential impacts across the sector.

In particular, she fears that private equity’s need to generate financial returns on a relatively short timeframe could hamstring operators and hold back investments that are needed to ensure the future success of the industry.

Senior living providers have been facing serious headwinds for several years, due to factors such as oversupply and historically tight labor markets. Meanwhile, providers are also looking to the future, and many have come to the conclusion that they need to upgrade their existing offerings and/or create innovative new models that will hold more appeal for future consumers — namely, the baby boomers. Juniper and some other providers are also devoting significant resources in order to position themselves to benefit from ongoing changes to the U.S. health care system, including to the Medicare Advantage health insurance program.

Private equity firms entering the space expecting to generate meaningful returns with a three- to four-year hold could find themselves stymied by these complexities. Their operating partners likely would bear the consequences, coming under pressure to maximize cash flow to pay debt service and increase net operating income (NOI) to generate an attractive sale price. This could create disruption in rental rates that would trouble other providers in the market; meanwhile, these PE-owned communities would not be making the type of long-term investments that are critically needed but would not start to pay off within the PE group’s hold period.

“This is certainly not everyone, but it’s something that we are seeing more and more, if you want to do large-scale renovations, not paint and paper and carpet, but if you want to reorient to building for the new consumer,” Katzmann said. “The way to push short-term gains is rate, occupancy and reduction in expenses, which is largely staff driven. And that doesn’t yield long-term results which impact, in my mind, the stability of our industry over time.”

Technology is one example she cited. Katzmann believes senior living providers must invest in robust technological platforms to both meet future consumer expectations and to play in the data-driven health care system. But this is an expensive and lengthy process, often involving initial investments in infrastructure to support elements like powerful WiFi, followed by the introduction of complex systems such as electronic health records that must be rolled out carefully over time.

Ryan Co.’s Ferguson believes that concern around private equity hold times is valid. She was successful in helping Titan make a play into senior living as a developer and private equity investor — the company recently sold two properties to a joint venture of Tucson-based provider Watermark Retirement and a global real estate investment manager. However, she left Titan because the company is de-emphasizing senior living in favor of other verticals such as multifamily and self-storage, where returns are realized more quickly, she said.

Ferguson also is seeing some private equity groups pressuring operators.

Few new senior living projects came out of the ground during the Great Recession, so communities that were built early in the recovery leased up quickly and were generating attractive returns in the high-20% range, she observed. As a result, many investors “chased this market,” which became overbuilt, and returns sagged into the low-20% range.

And for some private equity firms drawn by the promise of higher returns, their expectations do not reflect the current realities. In an effort to drive the financials that they want, they place the burden on their operators.

“They’re saying, we need to increase rents, we need to lower labor costs, we need to do all these things which may be unrealistic,” Ferguson said. “But, they’re putting in the pro forma to get the deal in the ground, and then they’ll just press and kind of hammer the operator to try to hit those returns as best they can.”

Other senior housing leaders have raised similar concerns. Private equity players in some instances are willing to pay high prices for properties that are not yet stabilized, betting on their future potential, executives with real estate investment trusts NHI (NYSE: NHI) and LTC Properties (NYSE: LTC) recently told SHN.

High bids are not only pricing out more conservative buyers but making it even more challenging for private equity to produce the returns they are seeking — and if an investment is failing to meet potentially unrealistic expectations, the PE owner might swap them out the operator in favor of another management company. Frequently shuffling management can compromise the resident experience and also undermines operators’ ability to build a stable portfolio, Ferguson noted.

The best operators … have already effectively chosen their dance partners.

Harrison Street Managing Director Mike Gordon

To avoid this scenario, best-in-class operators are selective about their capital partners and likely have already established strong relationships with private equity firms that have an appreciation for the challenges and complexities of senior housing and take a longer-term outlook, according to Harrison Street’s Gordon. His own firm was developing senior living projects even in the midst of the Great Recession, he noted, and counts well-regarded providers such as Houston-based Belmont Village and Baltimore-based Brightview Senior Living among its partners.

“I would say that new entrants to the space are going to encounter a bit of an uphill battle,” Gordon said. “The best operators with great track records, that are vertically integrated and largely coveted within the sector, have already effectively chosen their dance partners.”

This situation is pushing newer private equity groups to tie up with unproven operators, and Gordon anticipates that some of these partnerships will learn lessons the hard way, which will lead to some dislocation, particularly in markets where barriers to entry are not particularly high.

“It’s going to be interesting to see the dynamic of new equity, new debt and, frankly, new operators getting together and creating the wrong supply in the wrong markets,” he said.

Private equity upside

Despite her reservations about the current surge in activity, Juniper’s Katzmann does see a role for PE in senior housing. In fact, her son Andrew Katzmann is a senior analyst with Seattle-based private investment and development firm Columbia Pacific Advisors — a company that has an acute understanding of senior housing operations and was co-founded by industry pioneer Dan Baty, she pointed out.

That operational expertise is also emphasized by Columbia Pacific Managing Director Todd Seneker, who has led the development, acquisition and repositioning efforts of over 25,000 senior living units, in addition to overseeing activity in other real estate types for the firm.

“We generally assume a five- to seven-year timeframe, but I think we do a good job in our underwriting and are very real — we don’t pull all the levers to try to make a deal work,” he told SHN. “We engage our operators, whoever is the manager, very early. They’re right along with us and it’s a true partnership. We want their input.”

Similarly, Gordon touts Harrison Street’s close alignment with its operators, and the firm’s commitment to devising strategies that meet operators’ own business timelines and goals to be managing portfolios on a long-term basis. Harrison Street gathers and shares data with providers across its portfolio to inform strategy and operational improvements, and convenes its operating partners every year.

Make sure you’re on the same page in terms of what your goals are for the project.

NIC Chief Economist Beth Mace

“We have an ecosystem that’s been created over a dozen years, where our overall mandate is to do well by our investors as well as our partners,” Gordon said. “One of the ways of doing that is making them all better by sharing their broad takeaways, their strategies — that kind of symbiotic relationship that’s been created amongst all of us.”

Brightview in particular is a good example, he said, citing a recent transaction in which Harrison Street acquired a sought-after portfolio of 11 stabilized Brightview properties. Harrison Street and Brightview have had a relationship going back a decade, and have been in a joint venture for about the last five years.

“It came down not only to our cost of capital, but also the relationship that we had and our interest in really continuing to grow together,” Gordon said, referring to Harrison Street being rewarded that deal.

The Brightview properties were sold to Harrison Street by another private equity firm, PGIM, which had acquired 10 of them five years ago. Five years is a “minimum” hold time needed to deliver, lease up and season a senior living asset, in Gordon’s view.

The type of close operator alignment that Columbia Pacific and Harrison Street strive for is critical to making a private equity deal work in senior living, NIC’s Mace emphasized.

“The most important thing … is alignment of interest,” she said. “Make sure you’re on the same page in terms of what your goals are for the project.”

An operator seeking a long-term capital partner might not be a good fit for private equity, but there are open-ended funds that allow for long-term holds, Mace pointed out.

Ferguson also stresses alignment of interests as a critical component of private equity success, and she advises third-party management companies to carefully evaluate their agreements with PE owners. If the equity group has sole discretion to terminate the management company at any time, the operator may want to seek stop-gaps or compensation should that occur. And if the arrangement is structured as a joint venture, she recommends that operators seek to maximize their influence on decisions.

“In most cases, the private equity groups are bringing 80% to 90% of the equity, so the operator getting much say in anything is unusual,” she said. “But I found that sometimes when you ask for things to get you included in those conversations, they tend to be open to that.”

Senior living operators should also bear in mind that any capital provider — private equity or otherwise — will have timelines and priorities and will be subject to various market forces, Mace observed. So, a major upside of more private equity availability is that providers might more easily diversify their capital sources.

“Depending on where you are in the business cycle or the interest rate environment, in some instances the cost of capital is higher or lower for the public REITs, the private REITs, the private equity groups,” Mace said. “So, operators who have connections with multiple capital providers are somewhat protected.”

Mace and NIC as a whole are advocates for educating capital providers and senior living operators about available options and how to achieve sought-after alignment of interests. This is an effort that Gordon, Seneker, Ferguson and Katzmann all agree is of growing importance as new private equity capital continues to flow into senior living.

“I do think we have to address this issue,” Katzmann said. “It doesn’t mean that anyone or any organization or their objectives are wrong or bad, it means we have to put on the table the reality and decide what impact it’s going to have and what that means to us as an industry … I don’t know what the answer will necessarily be, but I think it’s a discussion we need to have in 2020.”

Companies featured in this article:

Brightview Senior Living, Columbia Pacific Advisors, Harrison Street, Juniper Communities, NIC, PGIM, Ryan Companies