As recession fears let up and historically low occupancy trends turn positive, the senior living industry may be able to rest a little easier about its prospects for 2020 — but it shouldn’t rest on its laurels, either.

That’s because many of the disruptive forces that have molded the industry in recent years aren’t going away anytime soon, according to Beth Mace, chief economist for the National Investment Center for Seniors Housing & Care (NIC).

“Disruption is here to stay, if for no other reason than the fact that we’re shifting from the cohort of the greatest generation and the lucky few into the baby boomers, and they are known as a cohort of disruption,” Mace said Wednesday during a Senior Housing News webinar on the 2020 outlook.

A shift in demographics is just one of the many disruptors on the horizon. Other shake-ups may come from health systems making further inroads into the industry, or from the technology used in senior housing communities and among older adult populations. Those disruptors may well persist into the many years ahead.

“I think that we’re moving into a decade of disruption, quite honestly,” Mace said.

And continued disruption is just one of the trends on tap for the year ahead. The U.S. economy is expected to keep growing this year, albeit at a slower pace than in 2019, Mace said. Low unemployment rates and wage pressures will undoubtedly remain a top challenge for operators — including Des Moines, Iowa-based LCS, according to President and CEO Joel Nelson.

“I think LCS is probably experiencing similar challenges across the space that other operators and friends in the industry are experiencing,” Nelson said, of the ongoing labor headwinds.

LCS President and CEO Joel Nelson

LCS President and CEO Joel NelsonWith regard to expected deal volume, this year looks similar to the last, according to Ted Flagg, senior managing director with professional services firm JLL (NYSE: JLL).

“I think the market feels the same going into 2020, [with] debt markets, agencies, still highly active,” Flagg said during Wednesday’s webinar. “We’re getting live price quotes now that are as competitive as I’ve seen at any point in 2019.”

Technology, health care disruptors

Rapid changes in both technology and how and where health care is delivered could transform the senior living landscape in the years ahead.

On the technology front, products from companies like Uber and Amazon could serve as an easy alternative to some of the services that senior housing communities already offer. And that, in turn, could make it easier for prospective residents to live in their homes for longer, requiring providers to rethink the senior housing continuum, according Flagg.

“We need to begin to redefine the way we think about the acuity spectrum, particularly at the lower end,” Flagg said during the webinar. “We may start to think about technology-driven, at-home services as the lower end of the spectrum.”

Another potential disruptor may come from the deepening trend of senior living providers linking up with health systems, as Toledo, Ohio-based Welltower (NYSE: WELL) did in its recently announced possible joint venture with Philadelphia-based Thomas Jefferson University and Jefferson Health.

Under that arrangement, Welltower would buy a stake in Jefferson Health’s real estate portfolio, which would allow Jefferson to more quickly expand its ambulatory care network and leverage Welltower’s data analytics to determine the best sites to build these centers. Meanwhile, Jefferson would also begin to provide more services to the roughly 20,000 residents of Welltower-owned senior housing communities in the Philadelphia area.

“I think the idea of building medical office and senior housing together, 10 years ago, was crazy,” Flagg said, referring to partnerships like these. “You’re starting to see that not only REITs, but the larger private owners, are looking for ways to work with health systems.”

That is perhaps not a trend that will widely materialize in 2020, Flagg cautioned. But, it’s one worth watching all the same.

In the near term, REITs will likely be net sellers of seniors housing, and likely net buyers of medical office and life science assets, he continued. That’s largely to do with the rise of algorithmic investment platforms, such as index funds, that are overwhelmingly focused on earnings growth.

Senior housing operators — while still a solid long-term investment — require more patience and attention than a medical office or life science tenant, Flagg said. And that makes them a near-term burden for some REITs.

“The thought there is that REITs have become more sensitive to earnings growth than ever, as compared to a focus on premium or discount to NAV [net asset value],” he explained. “I think the REITs will be less patient than private equity in comparison, around slow-growth senior [housing] assets.”

PE firms here to stay

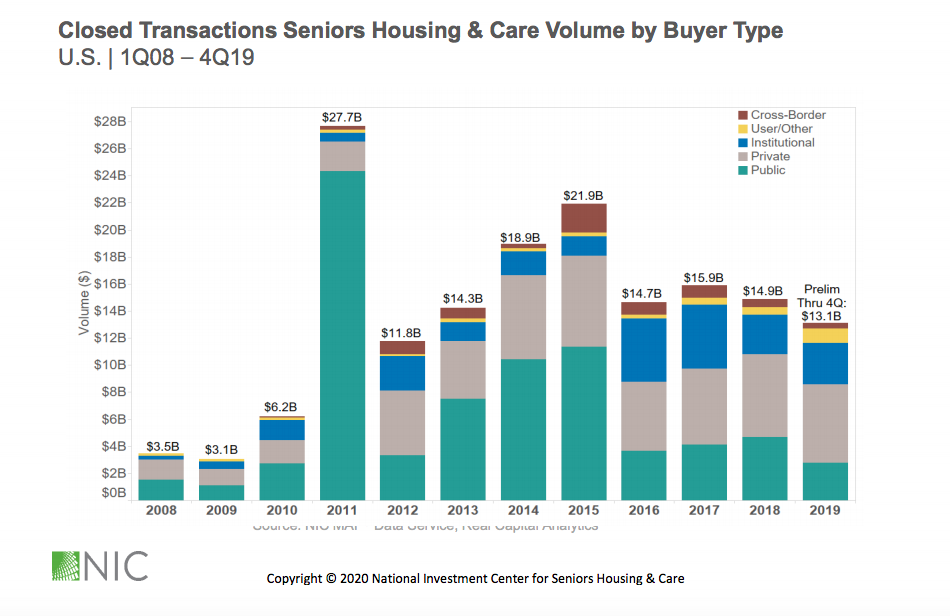

In terms of mergers and acquisitions, 2020 will likely resemble the three years prior, Mace believes. Since 2016, the industry has seen between roughly $13 billion and $16 billion in annual closed senior housing transactions, according to NIC data.

Supporting continued M&A activity, interest rates are likely to remain low, Mace said.

“A lower interest rate environment is important in terms of valuations for the senior housing market, suggesting that cap rates, if anything, are probably not going to rise significantly,” Mace said. “It also supports the acquisition environment with a lower cost of debt, and it keeps the cost of capital lower, as well.”

What is changing, however, is who’s spending all this money. In particular, private equity firms — which have become attracted to the senior housing space in part due to strong returns — are here to stay, Mace said.

“On a one-year basis, we saw investment returns for seniors housing of about 7.8%, which was significantly more than the 5.3% that we saw for apartments, for example,” she explained. “So, good returns is one factor that’s attracting private equity growth.”

Another factor attracting PE firms is the need to diversify their portfolios, as senior housing is often seen as a counter-cyclical asset type. There are also a number of emerging private equity firms devoted to senior housing, and institutional investors are becoming more comfortable with investing in the space as time goes on.

“I think one of the biggest challenges from an investor’s point of view, private equity or elsewise, is the lack of operators and property in which to invest,” Mace said.

At the same time, there is a “significant bifurcation” of pricing going on between the senior living and skilled nursing sectors, she added.

“We’re trading at about $191,000 per [senior living] unit, which is the highest that we’ve had since we started tracking this data in 2008,” Mace said. “Nursing care … is trading at about $83,000 a unit.”

In terms of timing, Flagg believes several large deals will be transacted in the first or second quarter of this year in an attempt to avoid market uncertainty surrounding the upcoming presidential election.

“We will have pretty good visibility as to what the year is going to look like based on what’s launched in the first half of the year,” he said.

LCS, for its part, is about two-thirds through spending the $300 million senior housing fund it announced with an institutional investment partner in 2018 — and is on its way to raising more, according to Nelson.

“We think there’s going to continue to be plenty of opportunity,” he said. “And we will put the capital in place and be ready for those times when they come.”

While LCS initially targeted life plan communities with the fund, it is now turning its focus to rental communities for the remaining one-third.

“That’s really where we’re focusing our efforts and our attention in 2020, to be able to look at those rental communities, preferably in a portfolio,” Nelson said. “But I think larger single site assets are something of high appeal to LCS, as well.”

Labor not a short-term problem

On the operations front, the labor market is expected to remain complicated and competitive, per usual. Hiring will likely remain tight through 2020 as record or near-record unemployment persists in many parts of the country.

“There’s only been two other [historical] instances where we’ve had unemployment rates lower than what we have right now, which is 3.5%,” Mace said.

Meanwhile, hourly earned wages for assisted living employees grew 6.2% in 2019, according to Bureau of Labor Statistics data. Assuming rent growth stays at its current levels of about 2.5% to 3% annually, that trend will complicate senior living companies’ bottom lines.

“There’s going to continue to be pressures on NOI, with expenses growing at a faster clip than what we’re seeing for rent,” Mace said.

Providers may also continue to have trouble recruiting workers, especially those on the front lines of their communities. LCS, for instance, is fighting a “wage war” over frontline staffers, and not even only with other senior living companies.

“We’ve come to realize this is not going to be a short-term problem, it’s going to be with us for some time into the future,” Nelson added. “We’re seeing pressures … within NOI margins, higher minimum wages, higher wage rates for some of the departments; leadership, staff, et cetera.”

To help on the labor front, LCS is pursuing multiple strategies, including by offering some executive directors equity incentives. The company is also trying to reach prospective employees when they’re still in high school by employing them as interns, for example.

“Being able to have that stock to offer to the executive directors who have chosen to stay the course … is a real advantage for us,” Nelson said. “[And], the earlier we can we can get students high school students interested in the opportunities in senior living … the more successful we will be.”

Still, even in the face of hiring headwinds, Nelson believes LCS is well-positioned for the future.

“We remain very, very bullish on senior living,” Nelson said. “I think [this year] will continue to be filled with disruption and complexity, and I think that will go well beyond 2020.”

Companies featured in this article:

JLL, LCS, National Investment Center for Seniors Housing & Care, NIC