Nationwide senior housing occupancy is near a historic low, as many providers across the U.S. are grappling with oversupply.

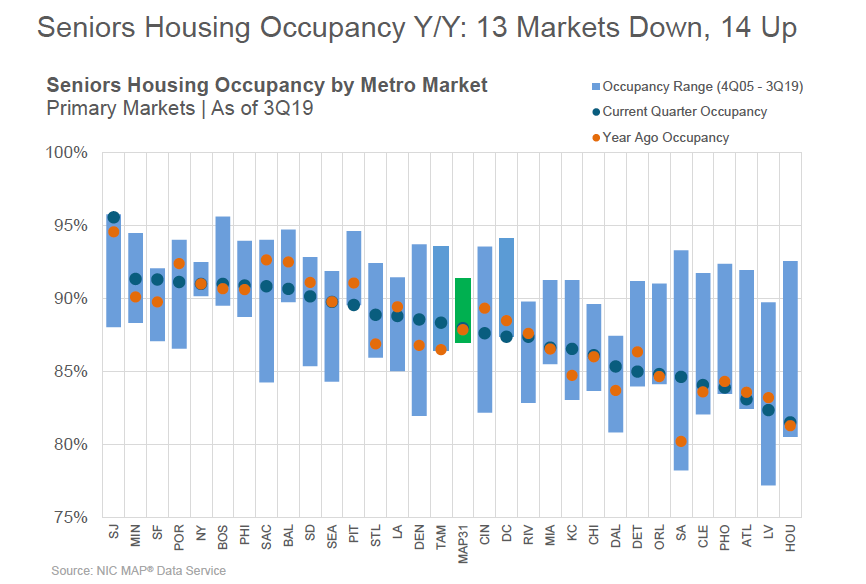

The average U.S. senior housing occupancy increased to 88% percent in the third quarter of this year, while construction versus inventory in the U.S. was 6.7%, according to data from the National Investment Center for Seniors Housing & Care (NIC).

But focusing on nationwide occupancy and supply doesn’t do justice to the nuances of the industry and to the individual markets themselves. Even in some of the nation’s lowest-occupied markets, such as Houston or Las Vegas, savvy providers still can carve out successful niches with some skill and luck. And in high-occupancy markets, achieving success is more complicated than “build it and they will come.”

A closer look at two specific markets drives home that point. Atlanta and Sacramento are both growing metro areas in areas of the country popular with older adults, but they are on opposite ends of the senior living occupancy divide.

Atlanta had an average occupancy rate of 83.1% in the third quarter of 2019, a decrease from the 83.6% average occupancy rate it had during the same time last year, according to the latest NIC data.

By contrast, Sacramento had an average occupancy rate of 90.8% in the third quarter of 2019, a decrease from the 92.6% average occupancy rate it saw this time last year.

While Atlanta is a significantly larger market than Sacramento, the two cities are growing at similar rates. The Sacramento metro area had an estimated 2.3 million people in 2018 and grew by 1.1% from the year prior, according to U.S. census data. The Atlanta metro area, which currently has an estimated 6 million residents, grew its population by 1.29% between 2017 and 2018.

To gain further insight into the opportunities and challenges for senior housing in these two metros, Senior Housing News connected with developers, providers, and industry experts, who weighed in on the particular factors underpinning the occupancy rates and gave hints as to where the markets may be headed.

Atlanta: Land costs high, rates tricky

Atlanta has seen a high rate of construction over the last several years because of market fundamentals and low barriers to entry. As a result, the market has seen relatively low occupancy compared to the rest of the nation. Construction is starting to tick down but is still occurring. In this environment, providers and developers say finding the right submarket is key, but that land costs and rents are making it hard for some to create projects that pencil out.

There are currently 231 senior housing properties totaling 21,792 units in Atlanta, with another 21 properties totaling 2,829 units under construction.

A low barrier to entry and steady demand in recent years have helped make the market a hotbed for new construction, according to NIC Chief Economist Beth Mace.

“Atlanta tends to be an area that just has strong population growth, so as a result there’s usually strong construction activity,” Mace told SHN. “And the ability to entitle land is going to be less restrictive in Georgia than in, say, California, so it’s easier to develop.”

But new construction is trending downward in the market. New construction was 17.3% of inventory in the third quarter of 2018, according to NIC data. One year later, it’s down to 13%.

The current senior housing trends in Atlanta are similar to the ones that played out in 2008, when the Great Recession triggered a similar slowdown in new construction. That may foretell an increase in occupancy there, according to Jacob Boss, a senior consultant with market research firm Plante Moran Living Forward.

“As long as absorption increases and annual inventory growth doesn’t go back up … I do see Atlanta’s occupancy ticking back up,” Boss told SHN.

The high rate of new supply in the Atlanta area has led to an uneven rate of success in that market, where some operators are doing well and others are struggling. Often, that varies widely among Atlanta’s different submarkets, according to Mark Maberry, an executive vice president with Formation Development Group.

“We found that if you work really hard to get into the right part of Atlanta or in the right neighborhood, you can do very, very well,” Maberry told SHN.

While the Alpharetta, Georgia-based developer doesn’t currently have any Atlanta projects in the works, it completed a 94-unit assisted living project this year in a suburb of Atlanta known as East Cobb. PGIM Real Estate bought the community for $43 million in September.

Looking ahead, Formation is open to additional opportunities in the market. But one roadblock to new development in Atlanta is finding land to build on at a cost that makes sense.

“We are keenly aware of how expensive it is to find land, and more importantly, how expensive it is to build new construction these days,” Maberry said. “Rents have gone up, but not commensurate [with costs], so, it’s getting harder to make deals that have the returns for our investors that they did years ago.”

Thrive Senior Living, which is headquartered in Atlanta, has moved a way from the market in part because it can’t command the right rent levels. Thrive only has one community in the market, a 95-unit assisted living and memory care community in nearby Roswell, Georgia. But that community was developed in 2014, and the company now undertakes projects in other parts of the country at a much larger scale — sometimes double that size.

“We’ve shifted our focus away from developing smaller assisted living and memory care buildings, and instead are developing larger, more complex, more expensive projects and demand premium rent,” Thrive Chief Investment Officer Alan Moise told SHN. “Based on those factors, we’ve been focusing on markets with historically higher rents.”

Pricing is an issue for many operators in Atlanta, according to Affinity Living Group CEO Charlie Trefzger. In particular, companies must balance rents that satisfy investors or owners with what prospective residents are willing to pay for senior living.

Add to the mix building age and location, and that’s a recipe for uncertainty.

“If it’s in a good area and it’s priced right, a community will do well,” Trefzger told Senior Housing News “If it’s a new property in a nice neighborhood but priced too high, it’s not going to do well.”

Hickory, North Carolina-based Affinity operates five communities throughout the greater Atlanta area and 143 communities across the Southeast U.S. The company’s strategy relies on offering senior living services at a rate that middle-income residents can afford.

In the future, there may be new opportunities to acquire and reposition properties in Atlanta. Affinity has a number of communities in the Atlanta area that are under contract for purchase later this year.

Trefzger sees a way forward in communities that serve the middle market — and there is a “great unserved” need for that product type, he said.

“The new buildings can’t compete with us because of their capital cost, and the cost to bring their communities to market are so much higher than ours,” Trefzger said. “So, we’re able to focus on that middle market with a more competitive capital cost.”

Although new development can be tricky in Atlanta, there are some seasoned companies making bets on the market. One such example is Heartis Buckhead, a forthcoming senior living community from developer Caddis in the Atlanta suburb of Buckhead.

As planned, the project will have 213 units when it opens in 2022. Integral Senior Living is on board to manage Heartis Buckhead.

Safer in Sacramento

Higher barriers to entry have insulated Sacramento from some of the challenges facing the Atlanta market, but the California state capital is also benefiting from some unique market dynamics.

Specifically, it’s seeing a steady stream of people migrating from nearby San Francisco, where residential rent prices are high and continually rising.

“Often, it’s a bleed-over from the Bay Area, and Sacramento benefits from that in terms of growth,” Mace said. “They’re also more mindful of construction and planned development there.”

Senior living owners and investors are well to continue targeting that market, provided they are willing to be patient and thorough, Boss added.

“If they can make the project pencil and they can get through entitlements, they’ll see the demand will be there because of the high barriers to entry that don’t exist in Atlanta,” he said.

Still, new construction is on the rise in Sacramento. The market’s construction versus inventory was 15.4% in the third quarter of 2019, an increase from the 13.8% it saw during the same period in 2018, according to NIC data.

There are currently 104 senior housing properties totaling 10,356 units in Sacramento, with 12 properties totaling 1,590 units under construction.

Contributing to that rise in new construction is Oakmont Senior Living, a Windsor, California-based company with 31 communities throughout California and Nevada, five of which are located in the Sacramento area. The company is currently undertaking two construction projects there.

Oakmont is able to succeed in Sacramento by fine-tuning its approach to different submarkets. For instance, while the company’s buildings are developed with a template, they’re rounded out with programs, services and amenities that are unique to the surrounding area, according to Matt Stevenson, a senior vice president of operations with Oakmont.

Oakmont owns its own construction company, OSL Construction, which helps the company have a better handle on the design and construction process.

“Sacramento is a great market for us because there’s so many distinct and unique submarkets,” Stevenson told SHN. “We’ve found a lot of success in this big market by … not cloning our buildings.”

Oakmont Senior Living

Oakmont Senior LivingFor its stabilized portfolio, Oakmont hovers at around 97% occupancy. At the same time, the company is the price leader in almost every market in which it operates, with average rates starting at about $6,600, Stevenson said.

While construction has indeed ticked up in the past year and change, Oakmont believes it’s well-positioned to increase absorption for its communities as competition heats up.

“We know there’s going to be an increase in supply beyond the supply we’re bringing into the market,” Stevenson said. “We don’t worry so much about the amount of new supply coming into the market as much as we worry about our ability to increase absorption.”

Solana Beach, California-based Senior Resource Group (SRG), which has three communities in Sacramento, sees the market as relatively “conservative,” according to CEO Michael Grust. But that could be changing as new entrants break into the market.

“At this point in time, we’re very comfortable,” Grust told SHN. “But sometimes a newcomer comes in and they have aspirations and then all of a sudden they start discounting rates. We’ve not been one to jump into that fray.”

Sacramento and Atlanta are just two markets among many in the U.S. But they show that, in the end, a quality operational model and community design can sometimes overcome market-wide pressures, and nationwide — even city-specific — occupancy numbers don’t paint a full picture of how promising or risky a given project might be.

Companies featured in this article:

Caddis, Formation Development Group, National Investment Center for Seniors Housing & Care, NIC, Oakmont Senior Living, PGIM Real Estate, Plante Moran Living Forward, Senior Resource Group, Thrive Senior Living