Some senior living providers that have succeeded on a private-pay model with robust margins are now starting their own Medicare Advantage insurance plans — diversifying into a complicated business with much thinner profits.

There is no simple explanation for why organizations such as McLean, Virginia-based Sunrise Senior Living and Bloomfield, New Jersey-based Juniper Communities are making Medicare Advantage (MA) plays. These companies are evaluating their operating models, markets, resident populations and trends in the U.S. health care system, and are laying bets that starting their own Medicare Advantage plans will pay off in multiple ways, financial and strategic.

To gain further understanding, analyzing a Medicare Advantage profit and loss statement is a good place to start. A sample P&L shows a thin profit margin, but also is a jumping off point to consider how starting a plan might boost the financial health of an associated senior living provider, while also being a more defensive play to protect providers’ interests in the longer term.

Breaking down the numbers

Under Medicare Advantage, private sector insurance companies receive funds from the federal government to offer coverage to Medicare-eligible older adults. If an insurance company designs its plans and manages care well for its beneficiary population, it can deliver needed services and payments while still having money left as profit.

Last April, the Centers for Medicare & Medicaid Services (CMS) announced that MA plans would be able to cover non-skilled in-home care for the first time starting in 2019. This policy change opened up the possibility that Medicare Advantage plans might start to directly reimburse senior living providers for some of their bread-and-butter services, ranging from assistance with activities of daily living to transportation and dining.

Juniper Communities founder and CEO Lynne Katzmann (pictured above) was quick to praise this shift in MA policy and has since spearheaded the creation of The Perennial Consortium — three senior living providers in the process of starting Medicare Advantage plans, with the administrative and logistical backing of a firm called AllyAlign.

In describing the Consortium’s strategy, Katzmann walked through a mock Medicare Advantage P&L at the recent National Investment Center for Seniors Housing & Care (NIC) spring conference in San Diego. She delved into further details in a followup interview with Senior Housing News.

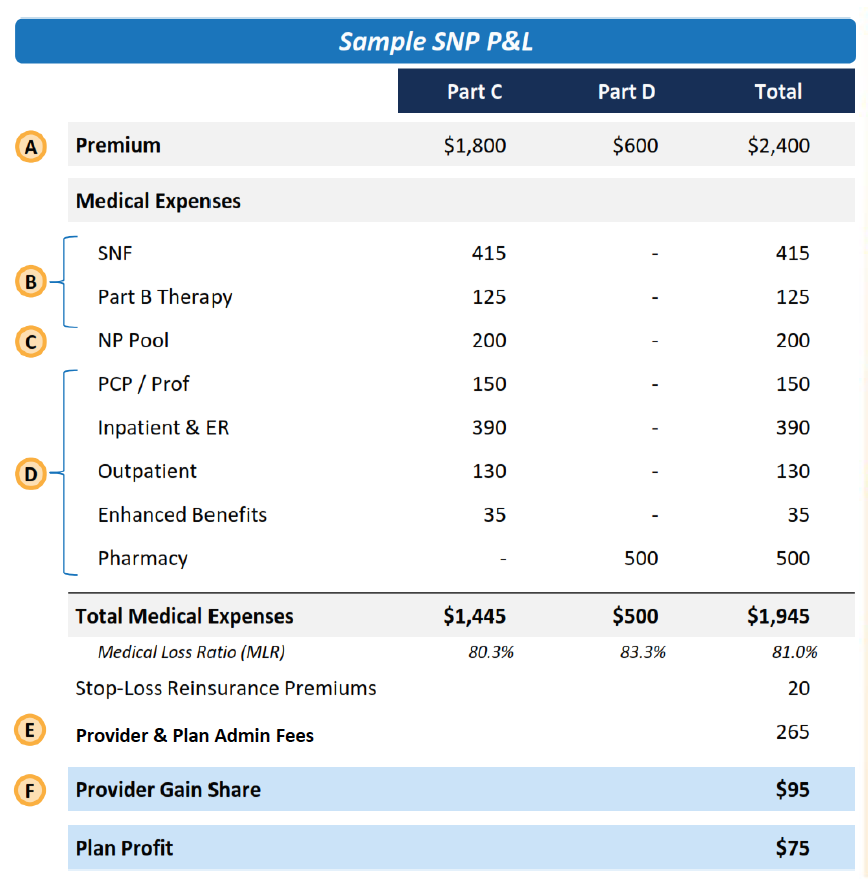

This sample P&L is from an institutional special needs plan, or I-SNP. There are various types of Medicare Advantage special needs plans, which were created to serve particular types of beneficiary populations.

I-SNPs are designed for residents of skilled nursing facilities; there are other types of special needs plans, as well as standard MA plans, which The Perennial Consortium may offer, Katzmann said. However, this I-SNP document provides a lens for understanding the basics of MA.

The premium dollars represent the amount that the insurer receives from the government on a per-member, per-month basis. The Medicare Advantage program is known as “Part C.” Because this plan offers a pharmacy benefit, the insurer also receives a Part D premium, bringing the total to $2,400.

The medical expense categories show what this plan pays out in benefits over the given month and are meant to illustrate plausible expense levels.

Most of the categories are self-explanatory, for services such as skilled nursing care and therapy; hospital care, including in the emergency room; primary care physician services; and pharmacy.

The “NP Pool” category is for care coordination services provided by a nurse practitioner. Ultimately, regulations might be relaxed as to who can provide these care coordination services, Katzmann believes.

The “Enhanced Benefits” category is worthy of special attention. These are the newly allowed supplemental benefits that CMS green-lighted last April. Currently, MA plans are offering these benefits on a small scale, but this could expand in the future.

As of now, these supplemental benefits are the only way that a private-pay senior living company would be able to get reimbursed directly by an MA plan, Katzmann emphasized. While she is confident that the amount will ultimately be higher than the $35 that is on this sample P&L, she is underwriting conservatively for now.

Katzmann is not alone in thinking these supplemental benefits could become more substantial than they are today. In fact, $500 a month is conceivable, according to John Rijos, who is a founding operating partner of private investment firm Chicago Pacific Founders and CEO of its senior housing platform, CPF Living Communities.

Beyond the dollars flowing to the senior living company through these new benefits, having an ownership stake in the other service providers listed on this P&L would also be a way to gain financially.

For instance, Katzmann has an ownership stake in Redwood Health Partners, which provides primary care in Juniper Communities buildings. By controlling the MA plan, The Perennial Consortium can ensure that the rate being paid for primary care is fair and sustainable for the Redwood business.

This is no small consideration. Medicare Advantage plans theoretically have an incentive to partner with high-quality providers across the spectrum of care and pay them a fair rate; in practice, this has not always held true.

For instance, skilled nursing providers have been under severe pressure from MA plans to shorten length of stay for residents — which reduces costs to the plan but also cuts into revenue for the SNF. Meanwhile, the SNFs are also being paid a stingier rate under MA than under fee-for-service Medicare.

And while it’s easy to lambast insurance companies for these practices, this sample P&L sheds some light on the bottom-line pressures driving them.

The P&L shows that with total medical expenses of $1,945 and additional administrative fees of $265, the insurer is left with $95 to distribute as gainshare to its partnered providers. Through gainsharing, health care providers in the payer’s network receive a cut if costs are kept under control.

This is another benefit to having an ownership stake not only in the private-pay senior living provider affiliated with an MA plan, but in the Medicare-certified providers working with it; gainshare can only be distributed to organizations that have a Medicare certification, Katzmann emphasized. Thus, Juniper would not be eligible to participate in gainsharing but Redwood would be.

A concept known as the medical loss ratio (MLR) further complicates matters.

MA insurers are required to spend 85 cents on the dollar for actual benefits that go to the consumer, so in a best-case scenario, a plan would start with a 15% margin, and from there subtract administrative costs and gainshare.

The margin shown on this sample P&L, of about 3% to 4%, is what the Perennial Consortium foresees as reasonable, Katzmann said. By way of comparison, the operating margin of assisted living communities generally was around 29% in 2017, according to the annual State of Seniors Housing report.

Beyond the margin

With these numbers, it’s clear that senior living providers should not expect to turn a huge profit on a Medicare Advantage plan.

However, starting a Medicare Advantage plan could shore up the fundamentals of the related senior living business, including through more robust referral streams and increased length-of-stay.

Since launching Sunrise Advantage, its in-house MA plan, Sunrise Senior Living has seen physician referrals increase 300%, CEO Chris Winkle said last December.

Doctors and other providers that are heavily reimbursed by traditional Medicare and Medicare Advantage tend not to think of private-pay senior living as a part of the care continuum, Winkle said in a Leadership Series interview with Senior Housing News last year. By becoming an MA payer, Sunrise gained a seat at the health care table, can highlight its ability to manage patient populations and coordinate services, and as a result, draws more referrals.

CPF Living Communities and its affiliated operating arm, Grace Management, have not started a Medicare Advantage plan. However, Chicago Pacific Founders has been investing in primary care provider groups that are managing services and assuming financial risk and upside for pools of MA beneficiaries. These primary care groups have begun referring some of their patients to CPF Living Communities, Rijos recently told Senior Housing News.

“The primary care doctors … said, Jane Doe, you need to live in a more congregate care environment, and by the way, an affiliated company of ours owns three of them here in town,” Rijos said.

By offering an MA plan, a senior living provider might also increase residents’ average length of stay by improving their health and wellbeing, raising customer satisfaction levels, and easing financial burdens.

To financially succeed in Medicare Advantage, a senior living provider needs a robust care coordination program, so that residents who are also beneficiaries are accessing services proactively to manage chronic conditions and sustain their health over time. Care coordination thus prevents costly interventions that erode the MA margin — but also reduces the number of residents who leave the community for a hospital or skilled nursing facility and do not return.

By becoming high-touch care managers, senior living providers can also boost overall customer satisfaction by reducing the burden on residents’ families.

Currently, the adult child is often playing the coordinator role, quarterbacking care for a loved one in senior living by spending long hours on the phone with various health care providers and providing transportation to appointments.

By becoming the housing provider and also the administrator of Medicare Advantage benefits, the senior living company takes on this quarterback role.

“[Sunrise Advantage] really gives them the opportunity for one-stop shopping,” Winkle said during his Leadership Series interview. “We can help you administer the Medicare benefit as well as taking care of you.”

Being the quarterback of care, the combined senior living/Medicare Advantage company can help residents get the most bang for their buck, guiding them to tap into care and services reimbursed through MA. As a result, residents would pay less out of pocket for these types of supports and would be able to afford their senior living rent for longer periods of time. As resident acuity has risen over time in senior living, this has become a more important consideration.

“Our markets, in certain areas, were becoming less strong because people can’t pay for housing and care,” Katzmann said. “MA becomes a potential new source of revenue to cover some of the care components.”

As senior living providers weigh the financial pros and cons of starting a Medicare Advantage plan, it must be noted that creating the infrastructure needed for success is neither cheap nor easy.

Consider the components that Juniper has in place. For years, it has been refining a Connect4Life operating model to support more robust health care services without sacrificing a hospitality-forward mindset. Doing so has involved the implementation of PointClickCare’s electronic health record platform; forging relationships with health care providers to offer wraparound services, including the Redwood primary care component that Katzmann herself has ownership in; as well as introducing new “care concierge” position in its buildings.

Now that all these pieces are in place, Katzmann and her Perennial Consortium partners are in the midst of an arduous process of designing and winning approval for their benefits packages. For each state where the Perennial Consortium is launching a plan, startup costs range between $3 million and $4 million.

Once a plan is up and running, it almost certainly will not make money in the first year, Rijos cautioned.

This is largely because the plan needs time to fully and accurately assess the needs of its beneficiary pool; based on this assessment data, CMS adjusts its capitated payments to the plan. So, assuming that starting pool of money increases over time, it becomes easier for a plan to achieve profitability.

This might all sound too daunting to take on, but it’s still very early days in the Medicare Advantage era for senior living. Providers that are interested in starting their own plan have ample time to get the pieces in place, Katzmann stressed.

Terminal value

Senior living providers that do not want to start a Medicare Advantage plan could go to existing insurers in their markets to become providers of choice or otherwise strengthen ties. Insurance companies such as Anthem and SCAN have signaled their willingness to have these discussions.

But Katzmann and Winkle see it as crucial for the industry that at least some senior living companies launch their own plans.

Medicare Advantage enrollment is increasing at a quick pace, and many of the behemoth insurance companies across the United States are growing this part of their business. These powerful insurance organizations surely will seek to increase their control over the senior housing industry, as they see how these settings are crucial to managing health care spending. Some observers have even predicted that an MA company will acquire a senior living provider in the near future.

So, now is the time for senior living providers to take control of their destiny by becoming insurers themselves, the thinking goes.

By starting their own plans, providers can create sensible benefits packages, manage the plans properly, and show the true value of senior living in delivering health outcomes and controlling costs. Having this information will be critical leverage when the big insurance companies come calling.

“I want to set a model, I want to share what senior housing can do, and have enough members in this program to set the stage so that when and if that happens, there’s an acceptable role for senior housing in this and the rug doesn’t get swept out from under us,” Katzmann said.

Her comment echoes what Winkle said in the Leadership Series.

“If we don’t do something here, we could wake up one day and find that we have a whole lot of managed care plans that are attempting to influence what we’re doing at the communities,” he said. “So the choice we made is, we’d rather drive that.”

When and if the big insurance companies do come calling, they very well might try to acquire the insurance entities created by senior living providers. Several of the large insurers have been open about their intentions to gain MA scale through acquisitions.

While Perennial Advantage plans have yet to even launch, and Katzmann has no intention to make a quick exit, she pointed to the attractive multiples of recent MA deals. This is one last and important financial consideration to make.

“The terminal value of the plan is really high,” she said.

Companies featured in this article:

AllyAlign, Chicago Pacific Founders, CPF Living Communities, Juniper Communities, Sunrise Senior Living, The Perennial Consortium